Insights from K-12 Superintendents on post-ESSER Investment Priorities

April 11, 2024 BlogWhile pandemic-driven disruptions to classroom learning may feel like they are in the rear-view mirror, new and ongoing…

Even as we sprint into a new year, this month we take a quick look back at the year that was in the education investment landscape. While much of the investment activity volume took the form of debt to support businesses through the pandemic, enthusiasm and interest in the sector remained strong. And, with considerable stimulus dollars supporting education institutions and workforce initiatives – and more anticipated – we expect the sector to remain an attractive, and relatively safe, harbor for disciplined investors.

With the flurry of current deal activity in the market, we expect you are staying busy. In a fast-moving market, clients value our time-to-insight and the efficiency with which we break down and assess the key investment considerations. We look forward to talking soon regarding your latest investment thesis or deal opportunity.

A Tale of Two Pandemics

2020 was the best of times and the worst of times for companies operating in the U.S. education markets. Place-based businesses like childcare and tutoring centers and summer camps were devastated by shelter-in-place orders, and enormous uncertainty led education buyers to freeze the purchase of anything that could be delayed (like textbooks). On the other hand, technology products and services that enabled education to take place remotely or to bypass closed institutions experienced dramatic spikes in demand.

This stark bifurcation in demand, played itself out in the education investing markets as well. Various types of EdTech businesses experienced strong demand for their equity, while more analog businesses relied on PPP loans and other debt instruments to survive the pandemic. Investors piled into EdTech deciding that the acceleration in technology adoption across education markets prompted by school closures is unlikely to reverse even once the pandemic ends. 2020 was the year in which EdTech in the U.S. went from a Silicon Valley fad to representing an asset class to which institutional investors of all types demanded exposure.

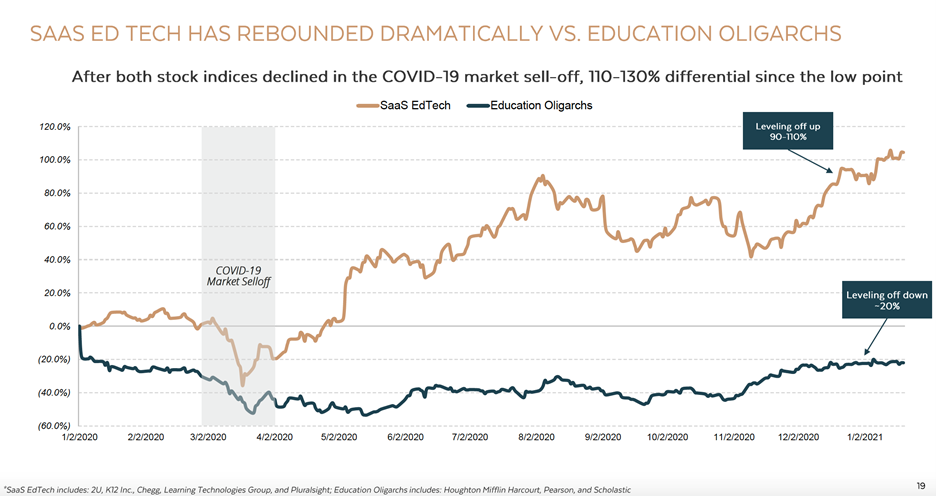

In the public markets this was evident in the performance of tech-enabled education stocks relative to their more analog cousins.

Further evidence of this enthusiasm is evident in the flurry of EdTech SPACs, including those aimed at investing in International, K-12, Higher Ed and Corporate markets, that have sprung up in the public markets. (NB: Tyton Partners has advised on a number of these efforts to date.)

Private market activity experienced a similar surge in 2020, with U.S.-based EdTech companies pulling in $2.2 billion in 130 equity investment deals (the biggest year on record) over $1.7 billion in 2019, according to EdSurge. But as with the stock chart above, the story for education companies generally – tech and non-tech — was far more mixed. According to Pitchbook data, equity investment globally across all types of education companies in 2020 declined 29% Y/Y to $7.7 billion. And while the number of transactions increased 42% Y/Y to 751, the volume increase in number of investments was entirely a function of PPP loans, with equity transactions (including early stage, growth and M&A) contracting sharply across all sectors.

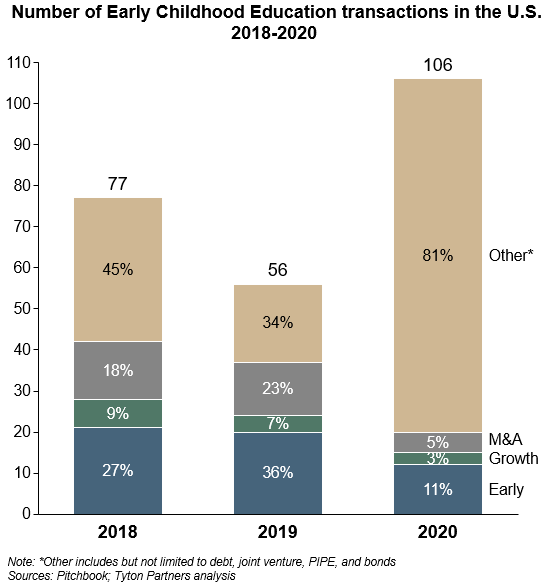

Early Childhood companies, largely built around place-based models, suffered the biggest declines in equity deals and the largest increase in debt financing (including PPP loans) to bridge gaps until facilities can re-open at capacity. Though some tech-enabled services have emerged, they are still striving to scale, and this market remains largely analog. While there was undoubtedly Covid-inspired innovation in this market, including Pods and online supplements, it was largely informal or otherwise fragmented.

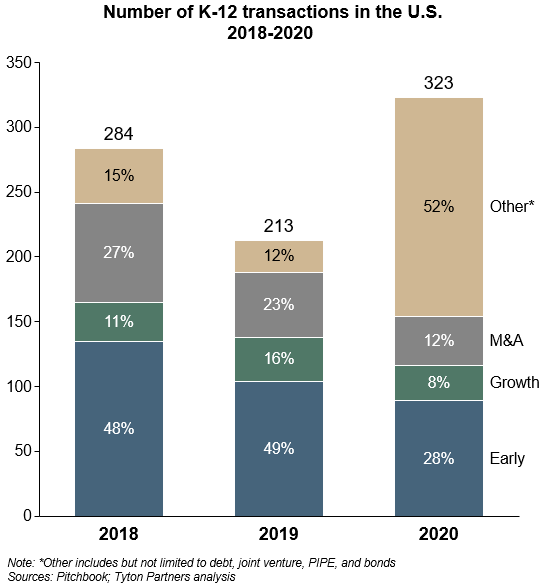

In the K-12 sector, the volume declines were less pronounced as surges in demand for consumer-facing and tech-enabled products expanded. Though down modestly, K-12 represents the sector with the highest proportion of early-stage activity, implying a far greater proportion of experimental start-ups than in other segments.

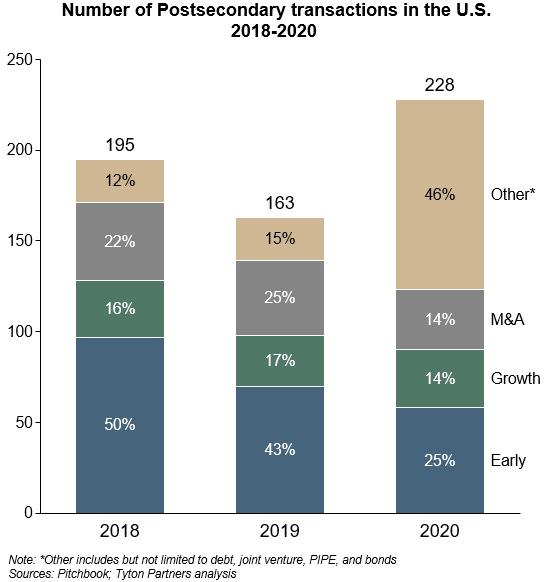

Among higher education-directed companies, the percentage declines were even more modest, with the number of growth investments modestly increasing Y/Y with investors keen to support companies’ ability to respond to consumer and institutional demand for tech-enabled products created as a function of the pandemic.

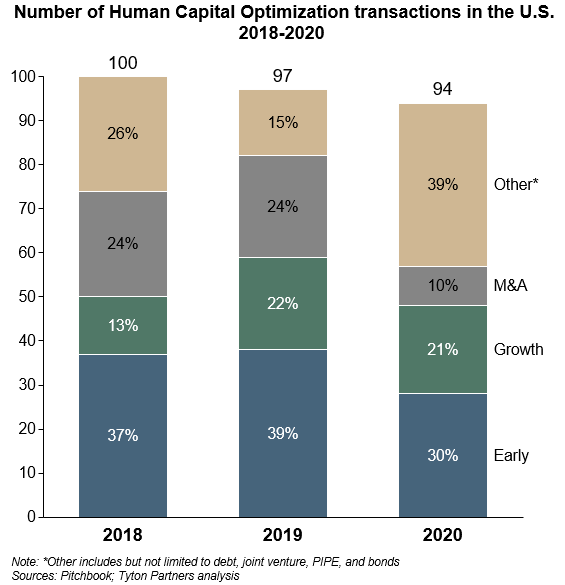

The decline in deals among companies focused on human capital optimization was nearly as steep as it was in early childhood. This sector, which includes both corporate-directed offerings as well as consumer-oriented companies focused on upskilling and re-skilling for shifting labor markets, includes a number of site-based businesses and faced the added uncertainty around corporate training budgets, which typically contract in recession. This softness was offset somewhat by new interest in remotely-delivered continuing education products and the substitution of online training and alternative credentials for what otherwise might have been post-secondary enrollment.

Overall, the new investor enthusiasm and belief in EdTech models is encouraging, and if vaccines allow site-based businesses to resume in-person operations by the second half of 2021, we would expect to see education deal volume to rebound dramatically over the next 12-18 months.

Recent Deals

PreK-12

Vistria Group Acquires Edmentum

Instructure Acquires Certica Solutions

Achieve3000 Acquires Teachonomy

Sanoma Acquires Santillana Spain

Genius Group Acquires Education Angels

NPM Capital Acquires Futurewhiz

Quad-C Management Acquires Learner’s Edge

Postsecondary

Kingsland University Raises $20M

Avallain Raises Undisclosed Amount

Penmark Raises Undisclosed Amount

Gryphon Investors Acquires Meazure Learning

Learning Technologies Group Acquires eThink

Human Capital Optimization

Performance Culture Raises $2.9M

iNSTRUCKO Raises Undisclosed Amount

Texthelp Raises Undisclosed Amount

Vista Equity Partners Acquires Pluralsight

The Access Group acquires Abintegro

Cerberus Cyber Sentinel Acquires Alpine Security

The Riverside Company Acquires Clinical Education Alliance

Marlowe Acquires DeltaNet International Limited

Learning Pool Acquires Remote Learner

KnowFully Learning Group Acquires The Income Tax School, Inc.