What We’re Thinking About in Impact for 2026

January 21, 2026 BlogThe education sector is navigating a fundamental shift. Market forces are driving consolidation, capital is more selective, and…

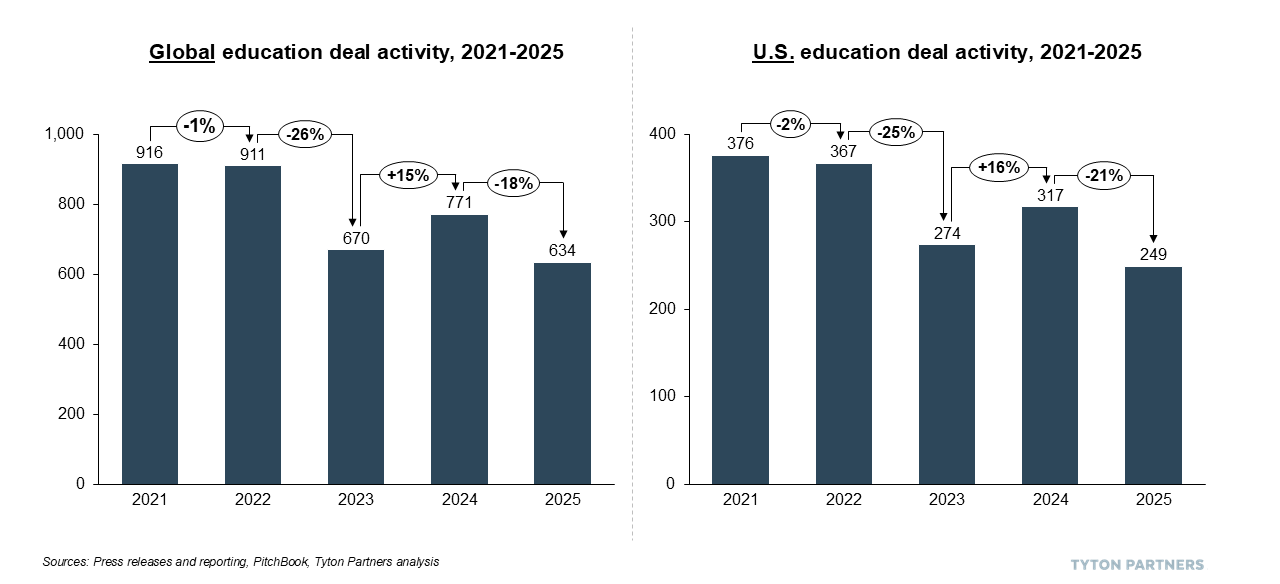

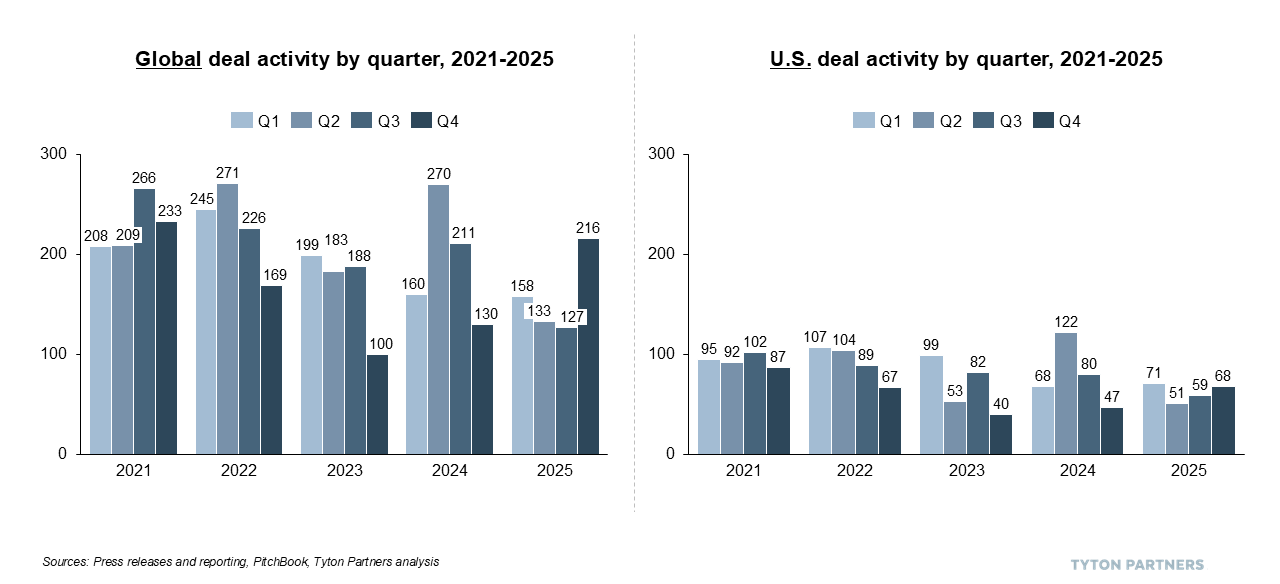

The 2025 rebound many expected after a partial bounce back in 2024 never materialized. Instead, global and U.S. education deal volume fell roughly 20% year over year—representing a ~30% dip from pandemic-era highs. This slowdown wasn’t unique to education—tariffs and other restrictive policies dampened investment across sectors, while elevated borrowing costs made it harder to justify bets on anything that didn’t have a clear path to accelerated growth or margin expansion.

Education did face a unique set of headwinds that exceeded expectations coming into the year. The Trump administration’s aggressive efforts to eliminate the federal Department of Education created uncertainty around funding, regulation, and procurement—particularly in K–12 and higher education (HED). Pandemic stimulus dollars ran out just as inflation lingered, tightening budgets. Meanwhile, enthusiasm for AI was tempered by caution: investors hesitated to back models whose pricing power and defensibility over five-plus year hold periods remain unproven with competing technology that changes so rapidly.

Taken together, 2025 was less a recovery than a reset—forcing sharper discipline on growth assumptions and widening the gap between durable platforms and fragile models. Still, select segments captured outsized investment, which we explore in the following analysis with an eye towards what 2026 will bring.

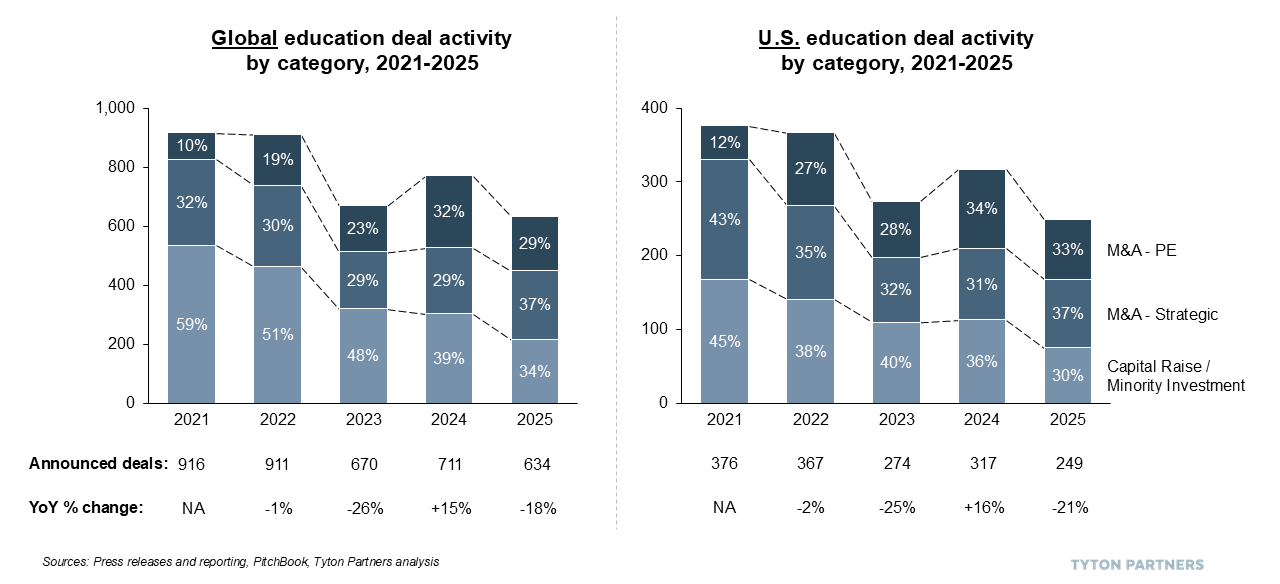

While overall education deal volume fell sharply in 2025, strategic M&A proved resilient—up 4% globally, compared to private equity activity dropping ~25% and minority investments plunging 29%. For operators and strategics, acquisitions became the go-to lever for growth, offering scale, capability expansion, and TAM extension without platform-level risk.

Strategic M&A activity skewed toward smaller transactions, with a handful of larger exceptions in higher education, including the break-up of Anthology—which filed for Chapter 11, refocused on its Blackboard LMS, and saw its SIS/ERP business acquired by Ellucian and its student success/lifecycle engagement units acquired by Encoura under a court-supervised restructuring. Other illustrative deals and rationales across the ecosystem included:

In 2025, strategic M&A wasn’t so much a bright spot as it was a necessity. Buyers used tuck-ins to unlock growth levers that organic strategies couldn’t reliably deliver: scale to strengthen market position, capabilities to deepen product ecosystems, and TAM expansion to capture new demand pools. With borrowing costs high and core markets slow, we expect this disciplined, purpose-driven approach to remain central in 2026.

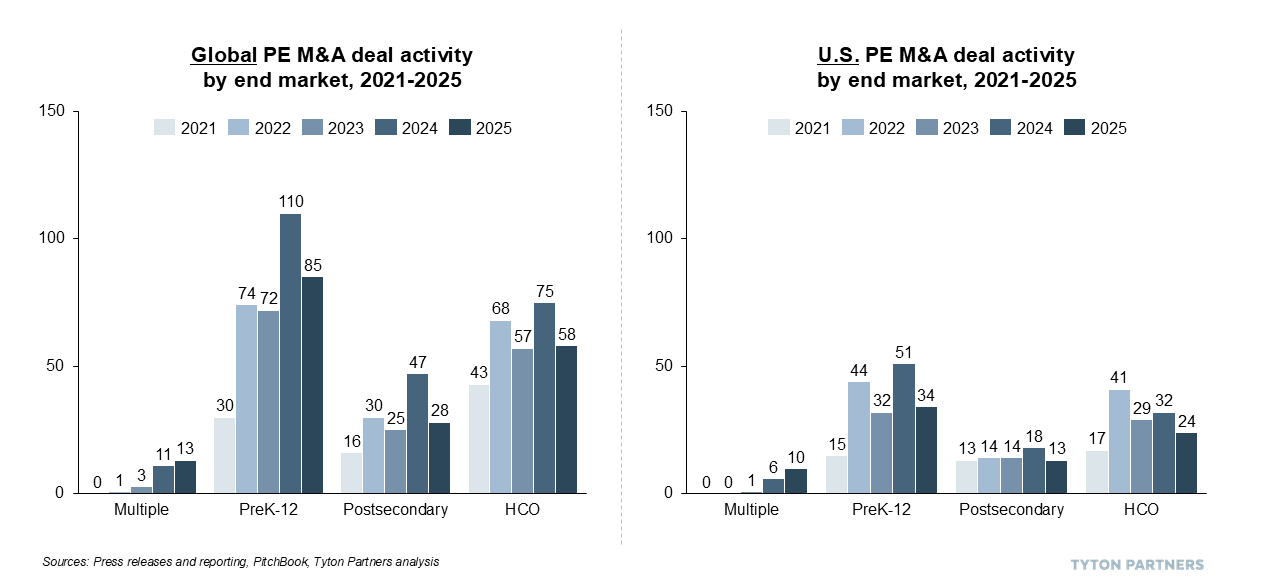

Private equity activity declined ~25% in both the U.S. and globally and across most end markets, as sponsors extended hold periods and adopted a “wait-and-see” posture. While partially explained by political disruption and resultant market headwinds, another sentiment we’ve increasingly heard is reflected in the following investor comment: “It just takes longer these days to generate the necessary growth to bring assets back to market and justify expected valuation. In some ways, six years feels like the new three.”

The upshot has been fewer quality deals coming to market. Even so, interest in deals remained high in 2025, funding was available, and capital still flowed (albeit in a more constrained way) toward segments viewed as more resilient. Noteworthy themes included:

PE investment in 2025 largely converged around predictable, modest-but-positive growth stories. Exceptions remained, but the prevailing mindset shifted toward stability over “rising stars.” We expect this resilience-first allocation to persist in 2026 as sponsors continue to prioritize durability over growth-at-any-cost.

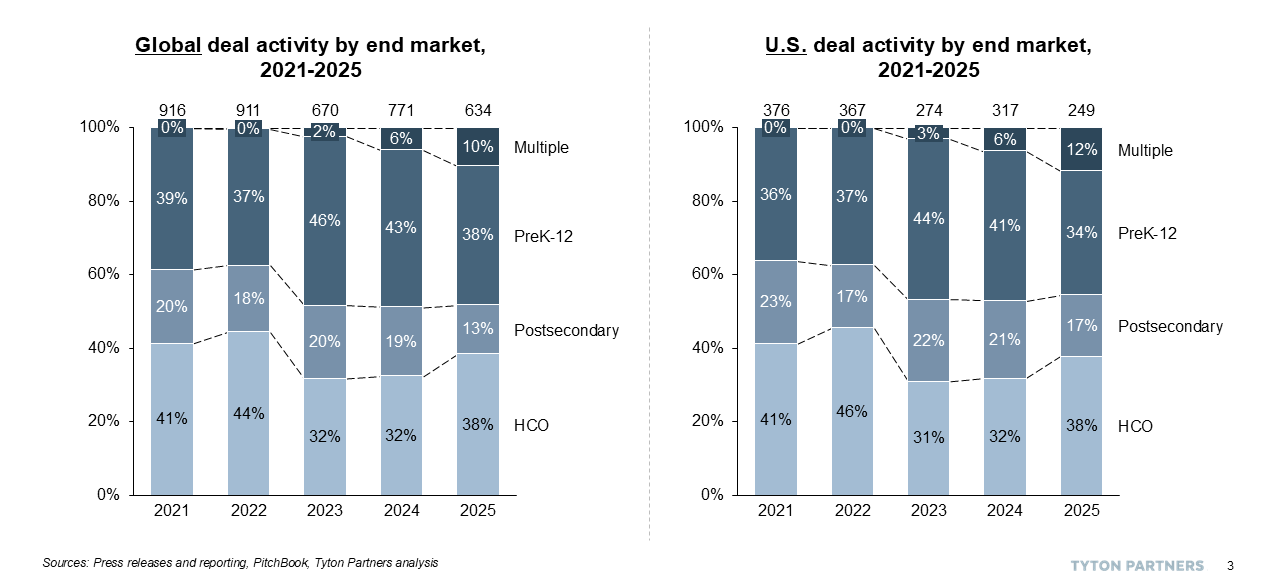

Deal activity declined across most segments in 2025, but the depth of the pullback varied. PreK–12 and Higher Education saw the sharpest contractions, with volume down year over year in both the U.S. (PreK-12: -35%; HED: -37%) and globally (PreK-12: -27%; HED: -41%). In contrast, Human Capital Optimization (HCO) proved comparatively resilient, capturing a larger share of overall activity despite modest absolute declines (-7% U.S., -2% Global).

A key driver of this divergence: relative stability of employer-funded spend versus public education dollars. As ESSER funding rolled off and per-student budgets tightened, investors shifted toward the “edges” of the education system – corporate learning, workforce development, healthcare training (along with early childhood centers referenced in the above section) – where funding sources are diversified and purchasing decisions are less exposed to state and federal budgets. Within these segments, several themes stood out:

In the “no hire, no fire” stagnant state the economy finds itself in, worker productivity will continue to win the day in 2026. While PreK-12 and HED should have weathered the worst of the storm and see volume pick up, we expect HCO investments to outpace those less insulated from political disruption.

2025 will likely be remembered as a year that hinted at improvement quarter after quarter—but never delivered—despite a global surge in transactions at the end of the year. As one US investor put it, “By August, we knew Q4 wasn’t coming and started building the 2026 pipeline. This was the earliest that’s ever happened.”

Expectations for 2026 are cautiously more optimistic, though few anticipate a breakout year. Borrowing costs are still elevated, but the trajectory may change as (interfering) pressure pushes for relief. Political volatility will persist, yet the midterm elections are expected to result in checks on executive power that could help restore stability. And budgets will remain tight, though planning should be more predictable than the post-stimulus whiplash of 2025.

In this environment, clarity – not acceleration – will define opportunity. Disciplined capital, strategic M&A, and a focus on durable demand drivers will remain central themes. Informed and thematic investing will win the day. If you’re exploring, creating, or refining your education-specific thesis, we’d welcome the chance to be a thought partner and to support your deal execution efforts.

*Tyton Partners tracks education sector transaction activity through various public and proprietary sources. All announced deals are reviewed to ensure accuracy of data and alignment with methodologies developed across more than a decade of monitoring the landscape.