Beyond Partnership: The Integrated Model of the College of Saint Benedict and Saint John’s University

August 20, 2025 BlogIn our second edition of Five for the Future: Spotlight on Transformative Institutional Partnerships, we turn to the…

The Bottom Line

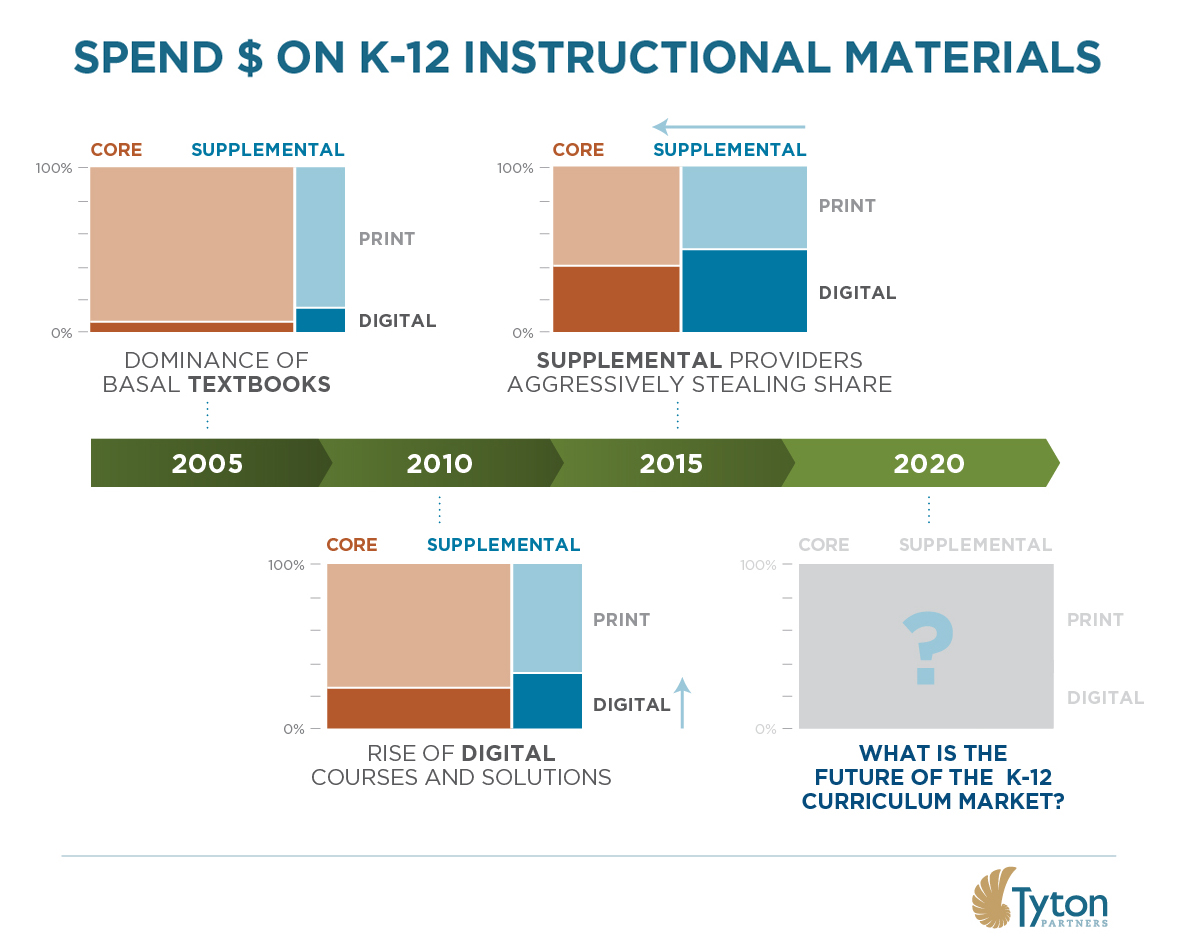

Poorly understood shifts in basal textbook spending, particularly in hard-to-track open territory states, have created confusion among large publishers and their investors as the market has become less predictable. And the shift to digital, which was once thought to represent a financial boon to the leading publishers, has instead created openings for supplemental solutions to steal basal share. Put another way, what is considered “core” from the perspective of the school buyer is shifting and creating uncertainty in a market once praised for its stability.

Over the past decade, Tyton Partners has been closely monitoring the more than $5B K-12 curriculum content market, analyzing shifts in the competitive landscape and exploring the forces responsible for painting new lines across this market. Indeed, the lines serving as boundaries between segments in this market – core (basal) vs. supplemental, print vs. digital – have become increasingly opaque, creating both winners and losers in the process.

The Rise of the K-12 Supplemental Segment

Over the past five years, leading supplemental solutions within the K-12 market have experienced impressive growth. Supplemental players have benefitted as schools and districts fundamentally change the way they use and purchase instructional materials:

Although historically perceived as lighter or less robust solutions, the overall depth, value, and perceived quality of supplemental solutions as a category has been increasing. Supplemental players are increasingly moving “up market” – seeking greater share of wallet and increased impact and mindshare within schools and districts – and are striving to position themselves as viable alternatives to more traditional (basal) textbook offerings.

Investor Interest, Company Transformation

Investors are displaying keen interest in the supplemental segment of the K-12 market, even as they have grown disenchanted with the K-12 portfolios of the leading basal providers. Two useful examples of supplemental companies receiving investment in 2017 – each at a different stage of maturity – highlight the enthusiasm in the segment and suppliers’ efforts to take share directly from the basal players:

Notwithstanding these – and other – supplemental players’ efforts, comprehensive curriculum offerings aren’t going away any time soon. However, we do expect many supplemental companies will grow faster than the overall market in 2018 and continue to replace more complete solutions, muddling market segmentation efforts. Increasing consolidation will occur in the supplemental market over the next few years, given recent (e.g., Edgenuity, Discovery Education) and pending M&A and investment activity, as these players expand into new subject areas and enhance or expand their own product offerings to drive increased value.

Visit with us at SXSW EDU

Want to continue the conversation? Let’s visit at SXSW EDU in Austin March 5-7. Click here to contact our team and set up time to connect or schedule a call in the coming weeks.

Tyton Partners has unparalleled expertise and insights into this dynamic sector – and others – within the Pre-K-12, postsecondary, and corporate / workforce learning markets. We do extensive client-specific market, product and customer analysis across these markets, and are always happy to share our perspective or answer questions to support and catalyze efforts at your organization.