Beyond Partnership: The Integrated Model of the College of Saint Benedict and Saint John’s University

August 20, 2025 BlogIn our second edition of Five for the Future: Spotlight on Transformative Institutional Partnerships, we turn to the…

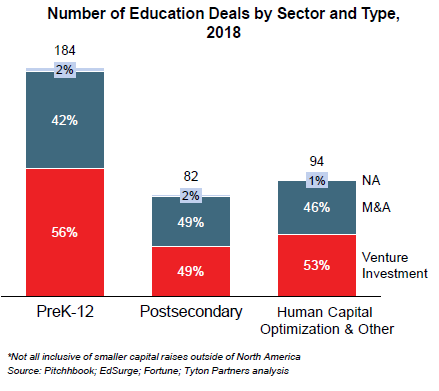

For this monthly deal round-up we took a look at knowledge services metrics from 2018. In the data we see evidence of a robust, vibrant, and perhaps most importantly, stable market. Venture and M&A deals are taking place in fairly equal quantities — suggesting steady maturation of winning approaches into sustainable businesses — and across all areas of the Knowledge Services value chain. And while the dollar value of these deals can vary dramatically (and in a relatively finite market distort perceptions,) we are encouraged by the general balance of activity.

Best,

Adam and Chris

K-12: Rising Dragons: Three (More) Capital Infusions in Asian Edtech

To U.S edtech investors, the numbers may seem staggering and even perhaps imprudent. Last month, three B2C online tutoring companies in Asia — Byju (India tutoring), Yuanfudao (China tutoring), and DadaABC (China ELL) — raised a total of $1.3 billion, implying a collective valuation north of $10 billion. These latest raises cap a year that also included $500 million for VIPKID (China ELL), $500 million for Zuoyebang (China tutoring), and $250 million for 17zuoye (China tutoring).

For perspective, we estimate the entire U.S. consumer market for education-related products and services is $16 billion, of which tutoring is roughly $9 billion. With that as a frame, it seems easy to dismiss the foreign investments as potentially overwrought.

But this assumption would be wrong. The Chinese ELL market alone we estimate totals more than $65 billion in annual spend, and the broader tutoring market is a multiple of that. In both China and India, the combination of a large, youthful population; high cultural esteem for education; and an insufficient public system make education one of the region’s largest and most vibrant markets.

Postsecondary: Emeritus & the Expanding OPM

India-based Emeritus closed a $40M funding round led by Sequoia India and with continued participation from existing investor Bertelsmann India. The company, which partners with universities around the world to bring their course content to corporate audiences, represents an interesting confluence of current trends in the OPM market.

Like Coursera and EdX, Emeritus brings short “certificate” courses to consumer and corporate audiences under its own branding, offering universities a low-stress avenue to ancillary revenue streams. However, unlike these recovering MOOCs, Emeritus does not dabble with the free or esoteric and in this respect seems to rival Trilogy, which has become the dominant player in the university-branded, employment-focused coding instruction market. Finally, Emeritus’s end markets are global in scope which means tens of millions of prospective new paying consumers of university content.

So while similar to other online university partnership models, Emeritus offers a unique combination of factors that is incremental to what others are currently providing. This combination of short, employment-oriented non-credit programs; global consumer and corporate buyers; and high-status university branded partnerships makes Emeritus an attractive target to OPM providers currently looking for new markets and new frontiers.

Human Capital Optimization: Human Capital Optimization — Lambda and the Expanding Boot Camp Market

Lambda School announced a $30M Series B round of funding led by Bedrock Capital, with Vy Capital, Google Ventures, GGV Capital, Y Combinator and Sound Ventures also participating in the financing. The new capital will be used in part to expand Lambda’s offerings in healthcare and cyber security.

While short, intensive courses in healthcare are uncommon, they are not unheard of and Lambda has suggested that it might consider acquiring a more traditional school and converting it for use as a bootcamp. What will be unusual however, is when Lambda introduces its ISA funding model to these types of programs, inviting students to take classes with tuition paid only after graduation and as a portion of their post-graduate income.

Many coding bootcamps are employing ISA funding models. (Lambda’s is 17% of post-graduate income for two years, not to exceed $30,000.) Few healthcare programs in a model like Lambda’s are taking this approach. But Lambda has made ISA funding a centerpiece of its marketing, signaling both affordability and accountability for outcomes to its students; this positioning will be something entirely new and potentially very powerful in the health care instruction market.

K-12

Moonbug Entertainment raises $145M

Providence Equity Partners acquires Tes Global

Veritas CapitalacquiresCambium Learning

Apex Learning acquires Youth Digital Project

Varsity Tutors acquires Veritas Prep

Houghton Mifflin Harcourt acquires Waggle

Centre Lane acquires Turning Technologies

Post-Secondary

ACTacquires American College Application

Grand Canyon Educationacquires Orbis

Human Capital Optimization