K-12 Predictions for 2026

December 18, 2025 BlogThe K-12 market has entered a period of structural change, driven not by a single shock, but the…

As higher education experiences a summer unlike any other, we wish you all a smooth start to the upcoming term. Please do not hesitate to contact us if we can be helpful as you manage and implement change.

We are devoting the bulk of our newsletter this month to the dramatic announcement from the University of Arizona that they are buying the formerly for-profit Ashford University and diving into the working adult degree market. With only this deal and the Purdue Kaplan one before it, we are hard-pressed to declare a trend. Yet we know from our work with institutions that many, many other public institutions are engaged in related discussions, performing their own buy-versus-build analysis as they consider how best to serve the online market. This deal, as announced, is not without controversy and we welcome your reactions to our thoughts below.

We also share this month the release of our annual Time for Class survey. Since 2015, Tyton Partners has tracked the state of higher education digital learning, courseware and digital tool adoption via Time for Class, the largest longitudinal study of faculty and administrators focused on digital learning strategy, tools, and practice.

Our 2020 release is designed for institutions and includes a series of short research briefs on targeted topics related to digital learning strategy, implementation of adaptive courseware, and inclusive access. Now more than ever, the use of high-quality digital learning strategies and tools is critical as we continue to navigate teaching and learning amidst a pandemic and work to ensure equity and access in student learning. You can download the full set of resources here. Please contact us to schedule a market briefing or to learn about how we can help you plan for and implement an effective digital learning strategy at your institution.

Best wishes,

Gates Bryant

Trace Urdan

Kristen Fox

University of Arizona Steps into the Ring

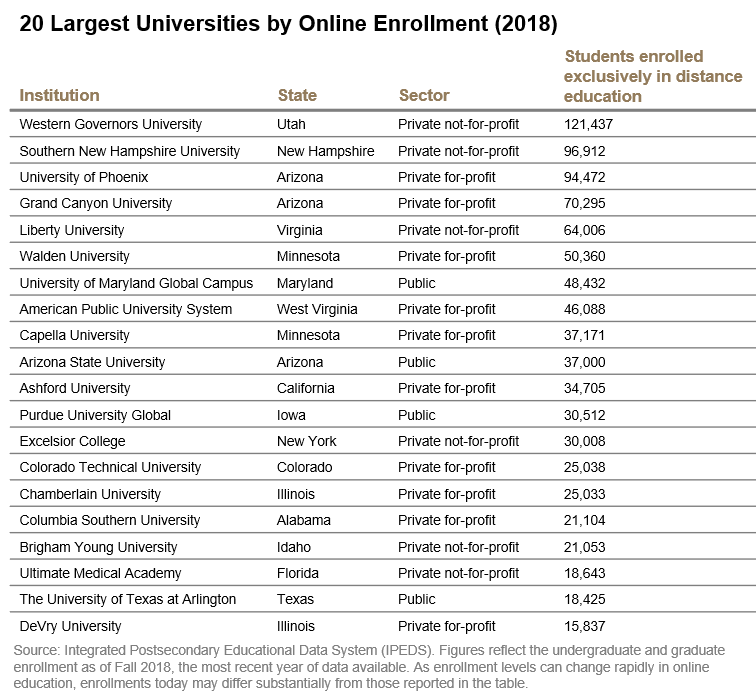

Last week, the University of Arizona (UA) announced that it had agreed to purchase Ashford University from Zovio (NASDAQ: ZVO) in exchange for $1 and a complicated contract for services with the seller of up to 15 years (what one might fairly describe as a rent-to-own arrangement.) The adult-serving online-only institution will move into a separate non-profit corporation affiliated with UA and will go to market under the title University of Arizona Global (UAGC). With approximately 35,000 students, the deal places UA into a small group of state institutions including Purdue, the University of Maryland, and of course Arizona State, that have large-scaled operations serving working adults on a national, and even international basis.

Zovio was in the midst of spinning Ashford back out of the company as a not-for-profit institution when it was approached by UA, which was keen to enter the undergraduate online market. The Arizona market is dominated by the University of Phoenix and its cousin institution Arizona State University (ASU), which itself has a large online population grown organically (though originally with its own for-profit partner Pearson.)

The contract between Ashford and UA is complex and is structured to ensure a financial return to UA Global, before Zovio as a service provider is even permitted to recoup its costs. Notably, Zovio has agreed to pay 1.5 years of UA Global’s revenue guarantee, or $37 million, up front and the state university has indicated that money will help to fill budget shortfalls created by COVID. Less clear in the arrangement is how much Zovio is obliged to spend to support the launch of the new school and whether the newly-christened entity will generate enough revenue and profit to make both parties whole. If the new entity outperforms, Zovio will experience the greater benefit, if it underperforms, UAGC will remain protected by the sum total of Zovio’s resources.

Whether you view the deal as more favorable to UA or to Zovio is a Rorschach test of how you feel about the growing presence of for-profit service providers in public education more generally. Criticism of the deal erupted almost immediately. Ashford had been a small, not-for-profit Franciscan school based in Clinton, Iowa before its purchase in 2005 by Zovio’s predecessor Bridgepoint Education, a for-profit education company backed by private equity firm Warburg Pincus, who grew it to a peak enrollment of more than 77,000 online students in 2012. Because of Ashford’s private equity origins and what many view as the cynical exploitation of an unwitting accreditor, it has long been viewed as a poster child of exploitative, profit-seeking in higher education and, fairly or not, has also been the pointed target of regulators and other critics of the sector more generally. This week, New America’s Kevin Carey, long-time critic of for-profit colleges and higher education services companies cautioned that students could be misled by the new branded entity and that the deal represents “an arrangement that obscures the lines between public and private interests.”

The truth, we think, is something more nuanced. Adults are currently underserved by public institutions in most states. Even those that have launched earnest efforts to provide online programs to adults are generally subscale and serve a relatively minor share of the adult students in their home region as compared to large, private, and quite often for-profit, out-of-state providers. Penetration by state institutions of adults 25-44 without a college degree ranges from only 6.6% in Maryland to 1.8% in Michigan. Additionally, a 2019 Eduventures analysis of IPEDS and NC-SARA data reveals that the number of states with more students attending online programs from out of state than in-state totals 15 whereas in only 9 states do public institutions have a better than 66% market share. (Interestingly Arizona has the greatest penetration by in-state institutions.)

The poor penetration by public institutions in the online market has less to do with pedagogy or intent than business model. The operating structure necessary to achieve scale and effectively serve adults at a reasonable cost is antithetical to most public institutions. It requires constant starts throughout the year, uniformity of curriculum, structured instructional pathways, proactive student support and serious digital marketing with a full staff of enrollment counselors prepared to engage with prospective students that have many more questions and concerns about a wider range of issues than do more traditional students.

For most public institutions predicated on consensus, stakeholder-based decision making, creating something so alien inside the institution is extremely difficult, if not impossible. As a small, private institution Southern New Hampshire University (SNHU) accomplished this with spectacular success, but only because its previous model was facing an existential threat. For most established schools, creating programs around these vastly different systems requires building (or buying) something apart from the core institution where it can function unconstrained by the status quo.

Therefore, for a host of reasons both profound and profane, state institutions are beginning to enter the online adult market in a serious way. Their missions should demand better service to those in their state that could benefit from a degree, and the revenue opportunity in this large online market make it an economic imperative as well. Given those points and the fact that the market is already crowded with players naturally invites buy-versus-build analysis. And many schools, like the University of Arizona, are going to conclude that buying – particularly in an environment where a shifting regulatory landscape creates more motivated sellers – is the more prudent and even desirable course to achieve scale.

Contact us to learn more about how we can help you navigate this dynamic market.