Catalytic Capital: From Recognition to Action in Education-to-Workforce Investing

July 8, 2025 BlogThe education-to-workforce pipeline is under pressure – and changing fast. The World Economic Forum notes that employers around…

Despite the challenges still associated with gathering in person, this year’s ASU+GSV Summit was a great success, allowing old friends to reunite and adding faces to names for new ones. We were pleased to have had a large presence at the conference, including participation in several panels, and were glad to have met with so many of you. Below we highlight some of the more prominent themes we heard at the conference, as well as some observations about deal activity in the first half of 2021.

Digital content – Innovation continues at the most basic building blocks of educational content as the pandemic fueled an enormous new appetite for digital material at every stage of learning from early childhood through workplace learning. And investors can’t get enough. Publishers and platforms alike are hungry for new digital approaches to traditional curriculum, as well as non-traditional topics and new approaches to addressing the historically underserved. Tyton Partners transactions representing both conventional and unconventional educational content announced over the past few months include a growth investment by PSG in DigitalEd; the acquisition of ArtistWorks by TrueFire Studios, a portfolio company of Growth Catalyst Partners; the merger of Philanthropy University into OneValley; the sale of Mentoring Minds to Curriculum Associates and the sale of LitCharts to CourseHero.

Focus on workforce – Not surprisingly, there continues to be a large amount of energy around everything relating to workforce education. Financial and strategic investors want to invest in workforce content and technologies, and post-secondary institutions want to find ways to better connect with companies as both employers of their graduates and as sponsors of students. And among all of these players, assessing and providing job-ready skills and competencies in a way that accelerates placement with employers is top of mind. Two Tyton Partners deals were announced the week of the conference including American Public Education’s planned acquisition of government training provider Graduate School USA, and a $25 million growth equity investment by Leeds Illuminate in Product School.

Tutoring – The growth of virtual tutoring during the pandemic, the perception of Covid-related learning loss as a market opportunity, the high-profile SPAC merger with Varsity Tutors, and several site-based tutoring businesses coming to market has led investors to dig deeper into this market segment. (The first and second place finishers at the Summit’s annual company pitch competition, abwaab and PrepMedians are both tutoring companies.)

Enrollment management – The accelerating adoption of test optional admissions is creating ancillary challenges for institutions, not only in identifying and qualifying a diverse mix of students, but also in making the delicate task of balancing full-pay and partial-pay families more difficult. Dozens of young companies are emerging to bring solutions for this new era of student recruitment. The acquisition of Edmit by Vemo in May and the July capital raises for GradTouch, Full Measure Education, and Unibuddy represent illustrations of this new ecosystem of companies.

Services competition heats up – The announcement of new short course offering by Noodle followed fast by Coursera’s announcement that it will improve the terms of its OPM offering with university partners raised the question at the conference of whether the benefit derived by short-course platforms like Coursera and EdX was at risk of being reclaimed by their university partners.

Federal funding – The effect of previous and potentially future federal funding continues to be a primary topic for both K-12 and higher education vendors. The quantity of funds currently coursing through various institutions from COVID-19 relief measures continues to be considerable but opaque as are various funding propositions put forward in the $3.5 trillion budget reconciliation bill recently passed by the House, including a proposed $65 billion for student success programs at community colleges and minority-serving higher education institutions.

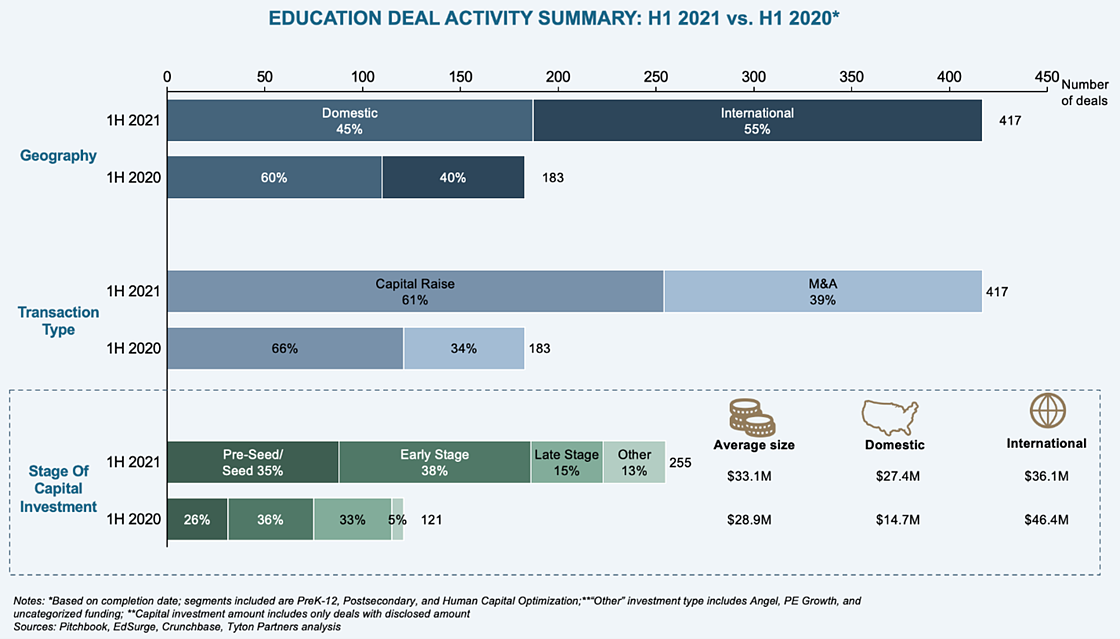

While the comparison might be an easy one given that it’s up against the scariest period of the 2020 pandemic, when a meaningful amount of deal activity froze, the first half of 2021 demonstrated growth across every possible dimension including quantity of transactions, dollars invested and average deal size.

Geography – The number of education deals grew both inside and outside the US, but grew internationally at a faster rate. Some of this is reflective of the relative immaturity of EdTech outside of the U.S., which tends to lead in most edtech markets (language training is a noted exception). Otherwise, the growth reflects the size of the Gen Z markets in India and China and the range of private-pay solutions for students seeking to improve their ability to test into limited public university spots. With the recent crackdown by Beijing on for-profit activity in the education sector, we might expect the rate of international growth to slow in the second half of the year.

Transaction Type – Though the markets experienced a slight uptick in control transactions, reflecting greater maturity and perhaps more anxiety about potential changes to the tax code, the greater emphasis on minority growth investments is a positive sign of enthusiasm and the runway perceived by investors.

Stage of Capital Investment – A greater proportion of early-stage investments likely reflects the uptick in exits mentioned above and again, should be viewed as a sign of sector health. The big story, however, is the growth in the average deal size in the U.S. which reflects both the volume of capital looking to be put to work, as well as the perceived opportunity for productive uses for capital.

All signs – both 1H deal trends and ASU GSV enthusiasm – point to EdTech as a meaningful new asset class for both public and private market investors. And with a resurgent COVID-19 strain and what seems likely to be new levels of Federal spending on all types of education, we expect the deal activity to continue through the 2H and into 2022.