Does Your Theory of Winning Actually Match the Market?

March 18, 2026 BlogIn competitive markets, companies don’t just compete on products or price. They compete on something more fundamental: their…

Over the last three months the U.S. K-12 market generated more than $3 billion of deal activity. As schools and districts transition back to in-person learning and experiences, they will nevertheless need to deliver more dynamic, flexible learning experiences and resources to retain and engage students. For their part, investors are active and optimistic about the role that suppliers will play in this process.

At Tyton Partners, we’ve taken a look back at historical investment trends relative to recent deal activity. The recent activity features notable themes, including large deal sizes in a market that historically has experienced more modest transactions, and a consistency among the investors that are engaged and active.

We’d welcome the opportunity to discuss the meaning and impact of these trends on all stakeholders with you directly.

Cheers,

Adam Newman, Managing Partner

Andrea Mainelli, Senior Advisor

Tanya Rosbash, Director

Investors Place Big Bets on K-12

The U.S. K-12 market has historically been slower growing and riskier than other education technology markets. For this reason, entrepreneurs must often go through more rounds of funding at early stages and have been less likely to persist to later stages. As a function of this, announced deals are often smaller in size. However, deals across the last quarter have demonstrated an increased appetite among investors for the K-12 sector, likely spurred by the disruptions of the last year. As schools, districts and families navigate the pandemic, investors are placing considerable bets on K-12 solution providers that will have a lasting impact.

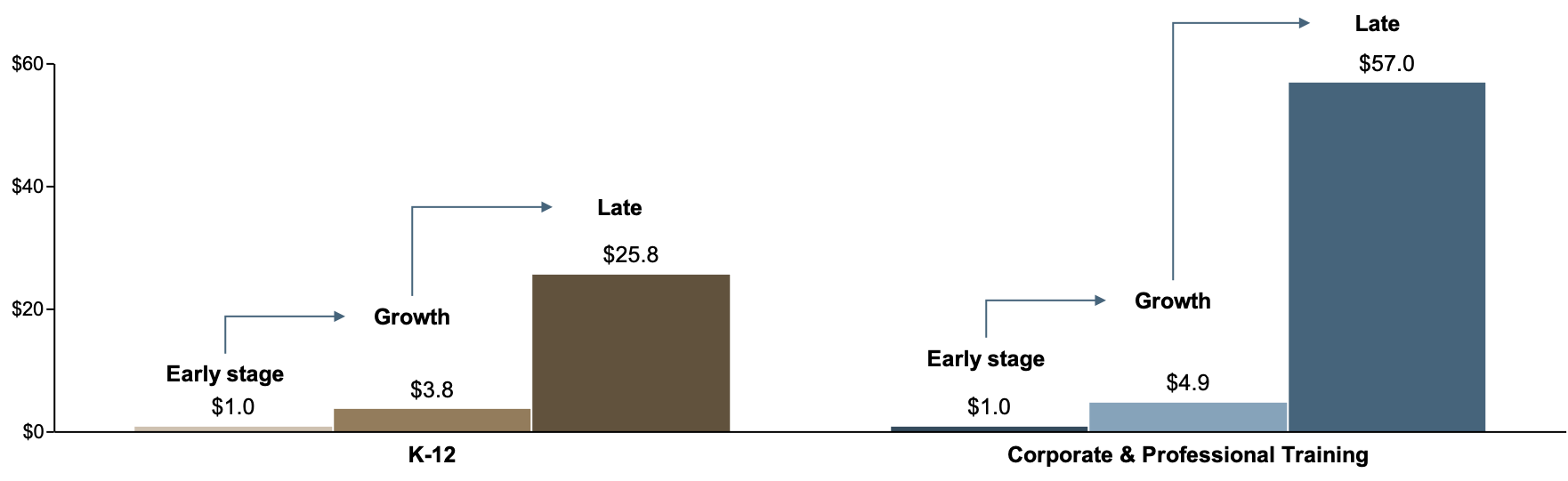

Over the last decade, companies in K-12 have completed an average of 1.8 early-stage deals compared to 1.2 in the Corporate & Professional Training (C&PT) sector. Median deal size in 2019 was $4M in K-12 compared to $11M in C&PT. Moreover, C&PT companies raise, on average, two times more in late-stage financing than that achieved by successful K-12 companies.

Capital velocity: capital raised in subsequent rounds for each dollar invested in early-stage deals*

*Based on a review of disclosed deal data from 2010 – 2020 in the U.S.

Q1 deals in 2021 reinforce two notable trends in the K-12 sector:

Moreover, with Powerschool planning to go public, Cambium currently in a sale process itself, and several other notable players also in – or rumored to be in – the market for sale, 2021 could shape up to be one of the most robust years for K-12 M&A and investment activity we’ve seen.

Selected Q1 deals

So what does this mean?

For entrepreneurs…

For investors…

The challenges for K-12 districts and schools striving to get out from underneath the pandemic are significant. At the same time, it has created a window of opportunity for both established and newer suppliers to find more, better ways to partner to help institutional customers, students, and families reimagine what can – and should – be achieved.