Reading the Education Market in 2026: Durable Opportunities in a Reset Environment

April 7, 2026 BlogA Market Adjusting to a New Baseline Last year, when we published our 2025 outlook, we were roughly 100 days into a new…

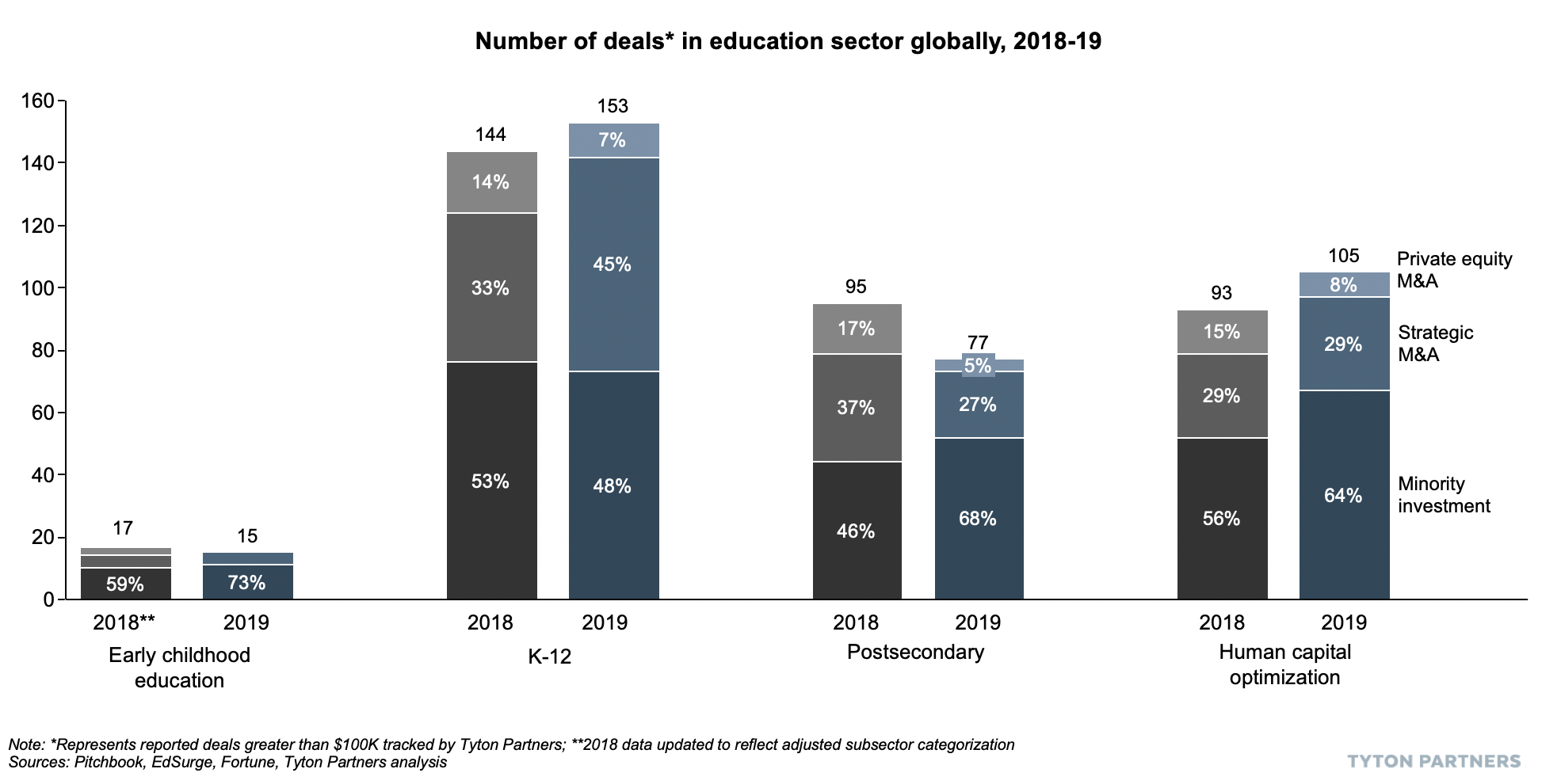

Happy new year and hope you have had a wonderful start to the 20’s. After tracking more than 350 deals in the education sector in 2019, we thought we’d take you for a quick spin highlighting the year’s key investment dynamics and deal volume. And, we offer perspective into what we see as continued areas of investor interest and activity in 2020.

At Tyton Partners, select illustrative banking deals in 2019 included:

On the consulting side, we completed a record number of diligence assignments on behalf of financial sponsors and strategic acquirers, culminating in our efforts supporting Wiley in its acquisition of mThree at year’s end. As we embark on the 10th year of Tyton Partners, we appreciate your support and look forward to our next deal working together.

We will be in London next week for BETT and Boston in late January for LearnLaunch. Let us know if you’ll be attending either, and we will find time to connect.

Cheers,

Adam & Chris

Overall, Tyton Partners-tracked deal activity volume was relatively flat in year-over-year, with more notable trends occurring at the sector level. Both K-12 and HCM saw an uptick in deal activity; strategic M&A was the key driver in K-12, while growth in minority investments was the HCM driver. Postsecondary experienced a drop in deal activity overall, even as the percentage of action shifted considerably toward minority investments.

Tyton Partners tracks industry deals through both public and proprietary sources.

Early childhood education brings the SaaS

Center-based childcare businesses have historically dominated conversations and activity regarding early childhood education investments. However, 2019 saw a pronounced shift into new areas, highlighted by two categories of SaaS software services: platforms designed to encourage program growth, and solutions aimed at streamlining and improving program operations.

The first category of platforms supports a general effort to democratize access to high-quality early childhood education programs in local geographies. Building on momentum generated by Wonderschool and WeeCare in late 2018, players like MyVillage and NeighborSchools received venture funding for developing platforms that allow stay-at-home parents to run licensed daycare centers out of their own homes. And in a similar vein, Kango, a ride-sharing app for young children and their caretakers reminiscent of Uber and Lyft, will get kids there – enhancing access or at least convenience – to childcare services in some communities.

The second category focused on center operations, is predicated on applying SaaS solutions to streamline management of various activities and reporting and to facilitate communication and outreach to children’s parents and family members. Warburg followed its 2018 acquisition of leading platform ProCare with a follow-on deal for Kinderlime, while newer players like Kangarootime generated investor interest. While it remains to be seen who may catch ProCare in this emergent segment, it represents a new enterprise SaaS ecosystem. And, with tens of thousands of center-based “storefronts” in the US and hundreds of thousands internationally, it’s only a matter of time before early childhood software players and investors start seeing some real unicorns.

Illustrative deals include:

Consolidation of SaaS administrative solutions and emerging niche plays

Tracing back to Vista Equity’s acquisition of PowerSchool and Thoma Bravo’s acquisition of Frontline Education, a key K-12 investment trend in 2019 was the continued consolidation of administrative SaaS tools for districts and schools. As we enter a new decade with the ubiquity of technology – and its related data “insights” – fully upon us, even public schools and districts are finally on-board. Most are embracing subscription-based SaaS models that provide efficiencies in compliance-driven record keeping and transactional business and administrative processes, while simultaneously delivering data analysis and reporting regarding district performance. As a result, incumbent platform providers and their investors are leveraging the inherent scale benefits of their distribution channels and accelerating rapid consolidation of administrative software businesses. Even as incumbents grab the spotlight, savvy investors made investments in 2019 to build new, competing administrative platform options for K-12 customers.

At the same time, new administrative niches continue to emerge as investors push to create platforms with critical mass in previously fragmented segments. A prime example is in the school safety area, where JMI’s late 2018 investment in school security software provider Raptor Technologies served as a platform for follow-on acquisitions in 2019. Other segments worth keeping an eye on include special education, social emotional learning, and health and nutrition management.

Illustrative deals include:

The great platform race

On the classroom side, the digital learning platform race is heating up. Contestants are staking their claim from every corner of ecosystem, including curriculum (e.g., HMH), assessment (e.g. ACT, Renaissance, Illuminate Education), and learning delivery (e.g., Instructure, NearPod). When paired with the fast-expanding administrative players (see above), we can expect a vibrant competition as we sprint into the new decade.

Illustrative deals include:

Incumbent publishers continue push across the digital chasm

It was a busy and challenging year for the postsecondary publishing incumbents in 2019. While the biggest news was the long-anticipated merger announcement by Cengage and McGraw-Hill Education (which remains “announced” pending anti-trust approval), the effort to transition to new business models was in full swing. Wiley was the most acquisitive, securing two innovative digital content platform providers – Knewton and Zyante (zyBooks) within weeks of each other in the late spring. While Wiley was buying, others launched initiatives striving to more fully capitalize on the market’s digital transformation, including bold new pricing models (e.g., Cengage Unlimited), revamped operational models (e.g., Pearson’s “digital-first” strategy), and accelerated adoption of inclusive access solutions. This disruption will continue to create opportunities for those capable of marrying customer-centric learning solutions with viable go-to-market strategies.

Illustrative deals include:

Enrollment slowdown drives deal activity

2019 was marked both by expansion and consolidation in the services sector as a slowdown in enrollment growth prompted a flurry of deal activity. Rapid expansion in the number of online graduate programs over the past several years among schools, both supported by OPMs and those operating independently, has prompted OPM providers and others type of services providers to look to both shore up and extend their range of services offerings.

Large incumbents have consolidated smaller players while adding to service strengths. Some of these themes have included adding digital marketing sophistication and capabilities and extending offerings into new areas. In the OPM landscape, providers have looked to grow their support of their university partners into non-degree offerings such as skills training and continuing education.

Illustrative deals include:

Alternative education models going mainstream

Short-term professional training programs (e.g., coding bootcamps, self-paced subscription content) were a hot buy in 2019, comprising nearly 20% of all professional education market activity as tracked by Tyton. Those pursuing differentiated models continue to prove attractive to investors, as demonstrated by Andela, which raised a fresh $100M to provide programming courses for aspiring developers in Africa; SV Academy, delivering sales and marketing training programs; and Kenzie Academy and Bitwise, seeking to meet the talent development needs of non-Tier 1 geographies. Two notable transactions – Investcorp’s acquisition of Revature and Wiley’s of mThree – highlight how the bootcamp model is pushing beyond simply training to deliver placement of entry-level IT professionals into various leading companies. We expect to see other staffing-oriented platforms enter the training space and an increasing amount of activity in the B2B digital skills development sectors as 2020 unfolds. Once dismissed as a fad, it seems very clear that short-term, private paid skills training has become a new permanent sector within the education market.

Illustrative deals include:

AI will take your job, and give you one too

Much like the traditional college textbook, the old models of employee recruitment are facing considerable transformation, slowed primarily by employers, hiring professionals and processes unwilling or unable to shift gears. Note – the old models will eventually succumb to the new ones. What this means today is that a sharp increase in bootcamp grads and those with “completion” certificates, matched by a rising number of employers looking beyond simply university degrees as a signal for candidates in a tight labor market, has made identifying qualified talent a challenging task. And that’s without considering the growing concern of unconscious biases in employer hiring practices. Consequently, AI-assisted talent acquisition and assessment platforms have been a prime target, not just for venture capital, but also for mergers and acquisitions. Ironically, the same technology that is causing angst for displacing workers, is increasingly responsible for placing them too.

Illustrative deals include:

PreK-12

Bertelsmann Acquires Penguin Random House

EdtechX Acquires Meten Education

Mentoring Minds Acquires SchoolSpire

Transom Capital Group Acquires Scantron

Higher Ed

BARBRI Acquires Kaplan’s Altior Group

EducationDynamics Acquires Thruline Marketing

GIGXR Acquires Pearson’s Immersive Learning Group

Science Interactive Group Acquires eScience Labs

Human Capital Optimization

Absorb Software Acquires ePath Learning