Prove it or Lose it: What it Takes to Win K-12 in 2026

June 11, 2026 BlogFor the past three years, our team has had some version of the same conversation: Is the K-12…

The Bottom Line

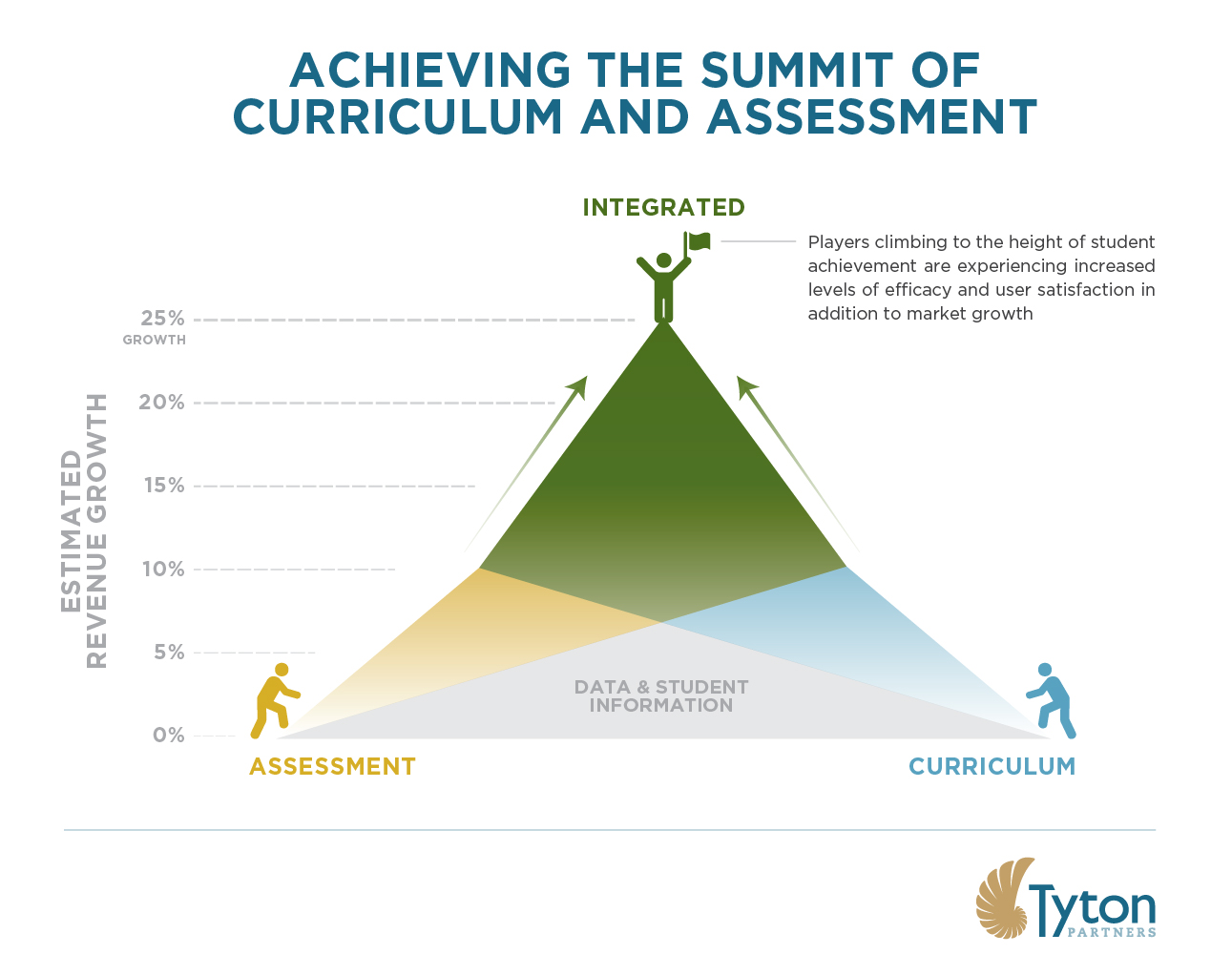

The assessment and curriculum markets have each experienced less than 5% CAGR since 2013. However, an emerging set of integrated offerings – those that tightly embed assessment within curricular offerings – have grown at 5x that rate. Are you playing in the right segment of the market?

Traditional assessment providers are struggling to gain market share in a slow-moving, highly-regulated environment, and curriculum providers are increasingly competing against freemium products, district and school’s DIY initiatives, and the market’s blurring of “basal” and “supplemental” offerings. Meanwhile, data-centric administrative and analytics players are striving to apply their “intelligence” to classroom interventions that can more directly impact teaching and learning. Companies and organizations in all of these segments need to respond to two near-term shifts in the landscape:

Bridging the Gap Between Assessment and Learning

Tyton Partners’ proprietary research reveals that more than 50% of school and district leaders cite alignment to instructional interventions and resources as one of the most important factors in selecting both benchmark and formative assessments. The marriage of assessment data and curriculum in the form of integrated offerings is what districts and schools want, as evidenced by the 5x growth rate of players in this segment. The convergence of the traditional assessment and curriculum solutions is a natural extension of the pursuit for enhanced differentiation – i.e., productivity for teachers and personalization for students – which leads to improved outcomes in the current K-12 market environment. Those who are not climbing this hill may find themselves increasingly left behind on the growth path.

Want more information?

Tyton Partners has unparalleled expertise and insights into this dynamic sector – and others – within the K-12 market and can help your organization chart its strategic path. We do extensive client-specific market, product and customer analysis at the intersection of curriculum and assessment, and are happy to discuss our broad perspectives if it would be helpful to your organization.

Click here to contact our team and learn more.