K-12 Predictions for 2026

December 18, 2025 BlogThe K-12 market has entered a period of structural change, driven not by a single shock, but the…

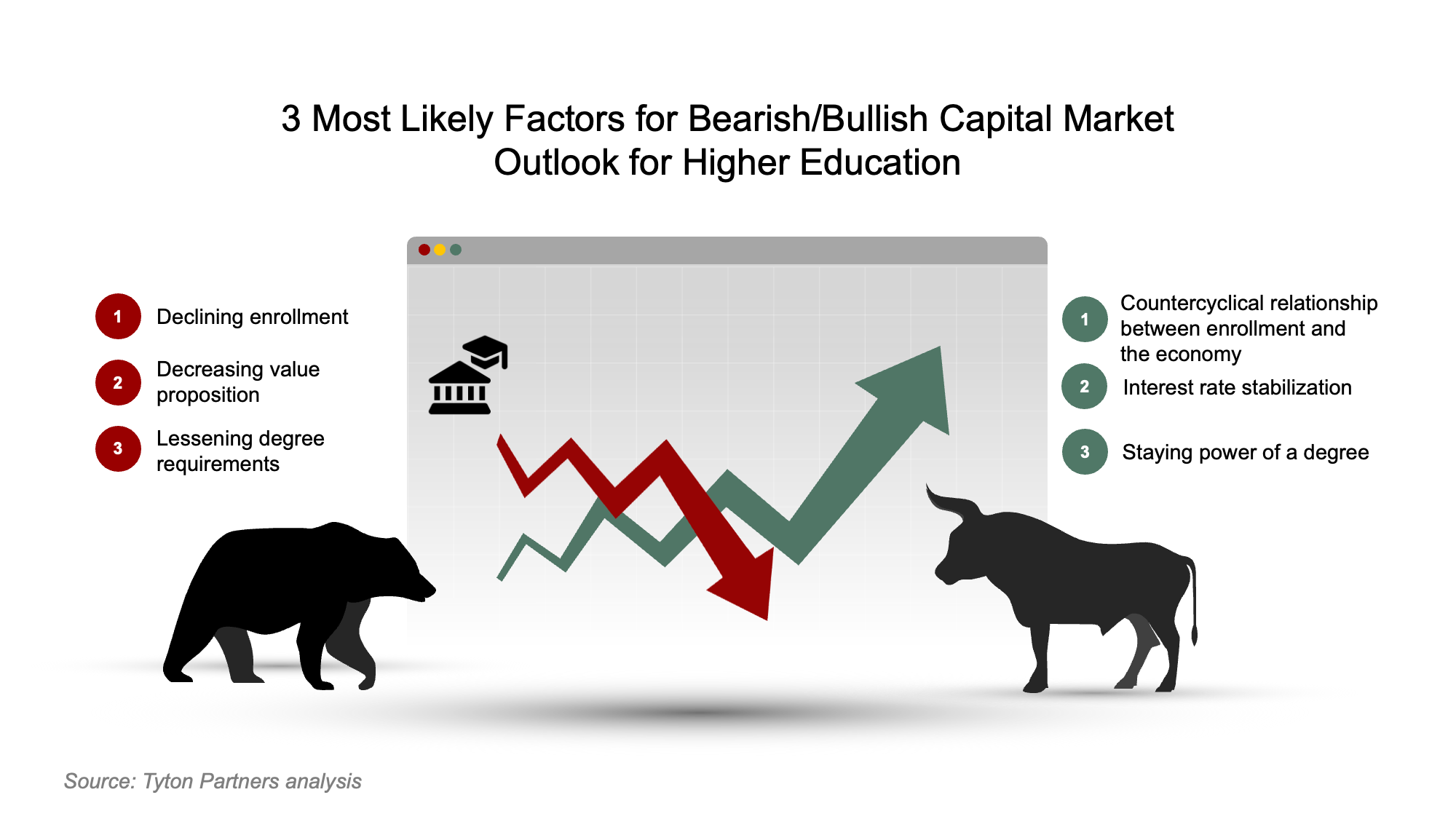

Bearish or bullish? Glass half empty or glass half full? Many factors influence one’s opinions on the direction of the higher education market for the remainder of 2023 and into 2024. Based on our observations and conversations with presidents, provosts, investors, and executives, we’ve distilled what we believe are the three most likely factors for either a bearish or bullish outlook.

A “bearish market” in higher education is driven by a variety of factors that negatively impact the financial outlook for institutions, and in turn, the established and emerging companies that support these institutions. This has been the most popular sentiment toward higher education over the past few years and is substantiated by institutions’ fiscal constraints, fewer technology procurements and delayed purchasing cycles. Unless a company has been working to tackle some of the problems expressed in this market outlook, you’re likely facing a tough year. Here are the three most likely factors for a continued bearish market.

While we’ve previously shared why the five-year enrollment outlook is less dire than some may suggest, U.S. demographics point toward headwinds for higher education for in the next decade. And over the past decade, undergraduate enrollment dropped by 15% (from 18.1 million to 15.4 million students).

As recently reported by the Wall Street Journal and the National Opinion Research Center (NORC) at the University of Chicago in March, 56% of Americans agree with the statement, “A four-year college education is not worth the cost because people often graduate without specific job skills and with a large amount of debt to pay off.” This reinforces a pre-pandemic trend as reported by Gallup, which showed the percentage of U.S. adults ages 18 to 29 who view college education as “very important” dropped from 74% to 41% between 2013 and 2019.

According to Cengage’s Graduate Employability Report, when asked whether a company requires a degree for all entry-level positions, the response changed from 62% to 50% in just one year from 2022 to 2023. This echoes the trend among employers, recruiters and hiring managers to focus less on pedigree – and the signal of a college degree – and more on experience, intent, inherent skills and potential.

Conversely, the bullish market outlook portends a more positive view on the direction of investments in higher education. Based on conversations we’re having with market participants, there is growing momentum for the following factors:

Conventional wisdom holds that enrollment trends are countercyclical to the economy. The COVID-19 pandemic, however, bucked this trend because of uncertainty regarding online learning and with job openings exceeding job seekers at historic levels. Yet, the job market has cooled, with nearly two million fewer job openings in the U.S. versus a year ago. And although the U.S. economy grew faster than forecasters expected at an annual rate of 2.4% in the second quarter, there are still lingering concerns of a recession. Many economists fear the ripple effects of interest rate hikes come with a lag. It’s possible that the pain usually associated with higher borrowing costs has not caught up with the economy yet. These ripple effects may be enough to return higher education to the historical trend of enrollment increasing as the economy worsens.

Despite the ripple effects concern, the general sentiment is interest rates have likely topped out, and there is a path – albeit a long one – to lower rates. Whether real or anticipated, a loosening of the Federal Reserve’s monetary policy and lessening inflation concerns will relieve downward pressure on investment returns. This will likely result in increased revenue gains from investment income and less, if not more predictable borrowing costs, and thus facilitate institutional, investor, and company fundraising and capital deployment.

Although students are becoming more skeptical, a degree is still worth it. For example, a bachelor’s degree is on average worth $2.8 million more than a high school diploma over a lifetime, according to The College Payoff, a report from the Georgetown University Center on Education and the Workforce – and the higher the level of educational attainment, the larger the payoff.

Moreover, there is an underappreciated reason college graduates earn so much more. It is not because they have an extra piece of paper. The wage premium for bachelor’s degrees reflects not state bureaucracies or corporate HR policies, but structural economic changes that generate more jobs requiring the experiences, knowledge and skills acquired in college. And it’s not as if institutions are standing still. While they can be slow to respond to changing market conditions, there is a push from policymakers for institutions to remain relevant as employers begin to emphasize skills over degrees in the hiring process. We regularly speak to institutional leaders who are moving toward career-readiness initiatives and skills-based hiring as a central feature rather than a missing final piece of a college degree.

So are you a bull or a bear? Regardless of which of these spirit animals your outlook most identifies with, we invite you to share your perspective. The factors at play are not mutually exclusive, nor are they exclusively influencing the direction of the higher education market and capital investment. We welcome your thoughts on what other factors we should consider.

Contact us at info@tytonpartners.com if you’re interested in discussing winning strategies that navigate the market outlook for higher education.