Behind the scenes of Otterbein University’s partnership with Antioch University

June 10, 2025 BlogWe’re excited to launch Tyton Partners’ new interview series, Five for the Future: Spotlight on Transformative Institutional Partnerships….

Last Wednesday, Joe Biden was sworn in as our 46th President. Discussions immediately centered on what the new administration would do to carry the nation to the other side of the crisis. His response was swift: a massive $1.9 trillion proposal that highlights direct aid to American institutions – among those, K-12 education, which has been allotted $130 billion.

Still, these figures are just headlines. While they are encouraging in scope and urgency, the Biden proposal must navigate a fractured Congress. As businesses navigate the spring selling season, we encourage you to push past the headlines to consider what we definitively know about the state of K-12 funding. To that end, we have outlined our current perspective on a set of key questions related to current and future dynamics.

If you would like to raise a question or simply explore these topics further, we welcome the opportunity to speak with you.

How much federal funding is required to stabilize K-12 education?

Note: Fiscal Year (FY) is based on a July 1st start. FY2021 equates to academic year 2020-21 (“this year”) and FY2022 is academic year 2021-2022 (“next year”).

Since the outbreak of the pandemic, budget shortfalls have plagued K-12. For months, politicians, administrators, teachers, and families have been calling on the federal government to provide more funding for states and, by extension, K-12. At Tyton, we have undertaken detailed efforts to square historical funding data with state-specific dynamics and expert insights to make sense of the K-12 funding dynamics.

Notwithstanding the complexities of K-12 state funding mechanisms and formulas, the logic behind the funding challenge for many districts is straightforward:

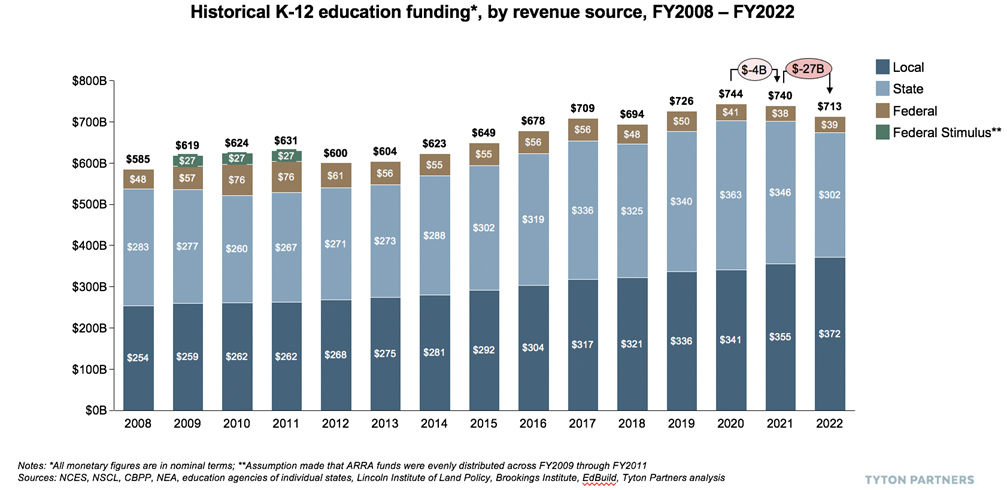

So how much funding does the K-12 sector need to overcome the deficit? During the Great Recession, state funding declined 2% in 2009 and 6% in 2010, warranting $80 billion in federal stimulus funding that worked to stabilize the sector over a three-year span. Today, if we had no funding from federal stimulus to-date, we estimate there would have been a state budget decline of 5% (-$17B) in FY21 and 13% (-$44B) in FY22. Our analysis indicates total K-12 funding would have declined by ~$4 billion in FY21 and ~$27 billion in FY22 – the equivalent of more than $500 per student. This suggests that the aggregate federal stimulus, inclusive of what has been provided to-date, will need to considerably exceed what was made available through the American Recovery and Reinvestment Act (ARRA) in 2009 to adequately support K-12 districts.

How does the path forward vary by state?

The funding declines are not felt consistently across the country – state and local dynamics vary, so context plays a vital role in forecasting K-12 budgets. Our team has created a state-by-state forecast based on state budget deficits, local funding formulas, and federal stimulus scenarios. The outlook for any given state is based on several factors, including:

These funding dynamics reveal that some states will fare better than others. For example, California – home to nearly six million students – is facing some of the nation’s most severe shortfalls in FY21-22. As such, the state is planning to defer $12 billion in K-12 district payments barring federal relief. Meanwhile, we expect a far more stable – and in some cases positive – outlook in states such as Pennsylvania and Alabama, where budgets have proven more resilient due to relatively consistent tax revenue and available rainy-day funds.

What has been the cumulative impact of stimulus funds already passed? Have they been “enough” to bolster K-12 budgets?

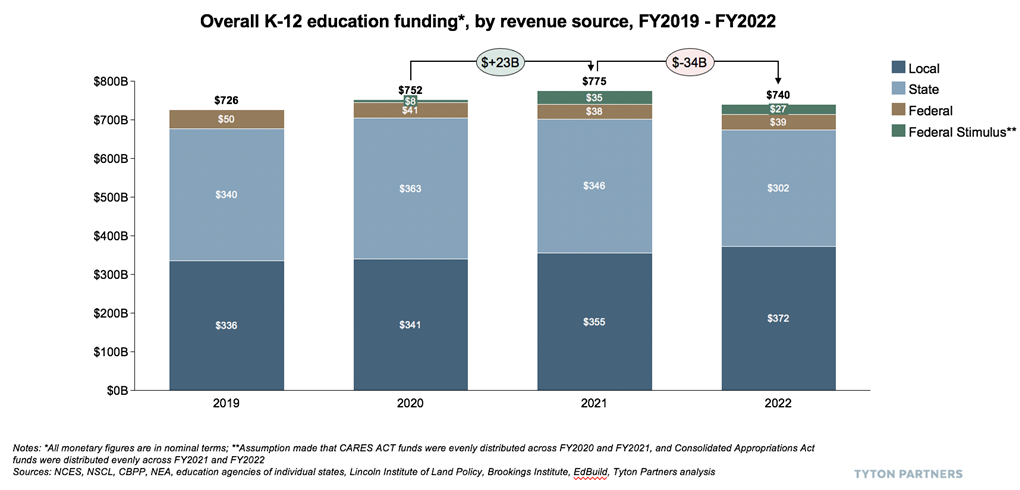

In response to the anticipated sharp decline in state budgets, the Federal government passed two relief packages directly allocating nearly $70 billion to the K-12 ecosystem. The CARES ACT was signed into law in March 2020 and provided ~$15 billion* in emergency relief; the Consolidated Appropriations Act (CAA), signed in December 2020, makes ~$54.3 billion available to K-12 through September 2022 and includes an additional $2.7 billion for private schools.

The impact of this stimulus funding on K-12 district budgets, spending, and student outcomes needs to be tracked across states and districts over the next two years; we estimate that overall, the stimulus funds will have a net positive impact on K-12 funding in FY21 relative to the prior year, driving up national totals by ~$23 billion, or three (3) percent.

However, without additional funding, these two relief packages will not be enough to keep FY22 funding at similar levels as FY21. We project there could be another steep “cliff” – this time more than $30 billion – should there fail to be additional relief. The Biden administration’s current request implies that the Federal government will step in with additional relief, but until that plan works through the challenging legislative process, questions will remain for K-12 district leaders regarding the resilience of their district budgets beyond this year. In a late 2020 Tyton Partners national survey of K-12 district leaders prior to Biden’s proposal, two-thirds of district leaders reported anticipating budget declines for the next academic year (i.e., FY22).

Proposed 2021 stimulus initiatives and other funding issues we’re watching closely

The new administration’s proposed stimulus is significant in scope. As it stands, the package allocates $130 billion to K-12 – nearly 2x what has been provided since the outbreak of COVID-19 and 1.6x what was made available through ARRA. As noted above, the package still needs to filter through the House and Senate, though, and early signs of the negotiation are emerging.

We are not going to speculate on the bill’s legislative promise; what we can do, however, is look ahead and consider how the K-12 funding landscape might change should a bill of this magnitude pass. Here are several issues we are watching closely:

Despite a number of open questions, the K-12 sector is on the cusp of what could be an unprecedented stimulus. Funding on its own will not solve all the challenges wrought by the pandemic and the crisis fatigue facing many schools and their leaders and teachers. It will, however, ensure dollars are available in the system to navigate the transition back to classrooms, focus on learning gaps and equity challenges, and in some communities, support a reimagining of school models.