Parents and students are attracted to 3-year bachelor degrees, but can institutions make the business model work?

September 23, 2025 BlogDifferentiation is going to be critical for colleges and universities to compete, and more than 60 are now…

One of the most memorable books I taught as a World History teacher was Stephen Greenblatt’s The Swerve. This book outlines how Western culture “modernized” through a spontaneous series of events. More specifically, Greenblatt argues that the chance encounter of an ancient text (On the Nature of Things) and the rise of the printing press in the 15th century catapulted new ideas into Europe’s mainstream, marking a turning point in history known as the Scientific Revolution.

As I read excerpts aloud from the front of an orderly classroom, desks in rows, the irony was not lost on me. We were exploring themes of social transformation within a classroom—and broader K-12 environment—that traces its origins to the Industrial Revolution.

Fast-forward to 2024 and we face our own pivotal moment. In the wake of the pandemic, pressures mount on the K-12 system: underperformance, absenteeism, and teacher shortages, to name a few. At the same time, the rise of parent agency, new state funding programs, and innovative learning models contribute to a new domino effect, one that could spark a structural shift in the K-12 sector.

As we look into the crystal ball and imagine what K-12 will look like in 2035, are we on the brink of a similar, more permanent “Swerve”?

A popular K-12 “doomsday” narrative has taken root. Headlines point to overwhelmed teachers leaving the profession and a generation of students in mental health and/or academic crises. But there is more to the story. On the back of these issues, parents, policymakers, educators, and business leaders are hatching responses, setting the course for a more dynamic future.

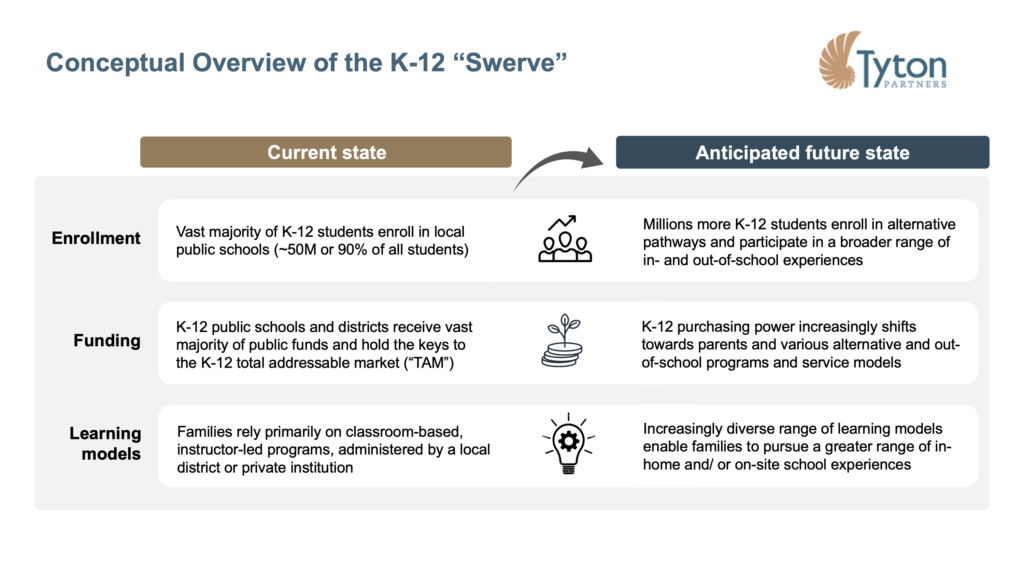

Consequently, the K-12 sector is on the cusp of transformation. Recent indicators suggest that in the next ten years, our system will undergo secular changes in what, where, and how students learn. Three main factors are driving this Swerve.

In the coming years, millions more students will enroll in alternative K-12 pathways (i.e. those outside a traditional public school system). Between Spring 2021 and Spring 2022, public school districts experienced an estimated 9% (or over 4 million students) decline in enrollment.

Our recent Choose to Learn research points to the persistence of this trend. 50% of K-12 parents are part of a segment “open-minded” towards education alternatives. With that, nearly 1 in 5 K-12 parents (17%) plan to switch their child to a new learning environment in the next 1-2 years (either by enrolling in an alternative school or selecting a more DIY approach). Even if this plays out for only a quarter of the 8 million students represented in this sample, we can expect millions of students to migrate to new learning environments.

Seizing the moment, states are delegating more ownership to parents. Programs such as Education Savings Accounts (ESAs, highlighted in our 2024 series Paying for Choice) and other microgrant programs enable K-12 parents to use public education dollars at their discretion. These programs now cover more than 20M students across 20 states (nearly 40% of K-12 families).

In turn, the total addressable market for students already eligible for ESAs and microgrants is well over $100 billion. This amount is expected to grow as more states introduce K-12 funding programs. Ostensibly, these policies allow “Open-minded” parents across all demographics to be more active consumers. This could result in a significant rebalancing of where and how spending happens across K-12 institutional and consumer markets.

Providers are offering more “flavors” of education that cater to a broader range of student interests and outcomes. As new models continue to crop up, both within our public school system and outside of it, K-12 families will encounter more options than ever. In this environment, K-12 districts—long viewed as stalwarts of the status quo—have an opportunity to become change agents.

Outside the system, a wave of innovation is taking root; in Florida alone, 250 microschools opened their doors in 2023. Benefitting from new regulations that make it easier to launch and operate new schools (and buoyed by parent demand) the landscape of K-12 learning models will continue to diversify.

Overall, we expect the K-12 sector to experience systemic and structural changes. As these dynamics take root, what should you do?

As one sales season leads to another budget cycle, it can be difficult to elevate your gaze to catch sight of the horizon. Even seasoned K-12 business leaders can find themselves focused on where the market is now, rather than where it is headed.

Challenge the “business as usual” mentality and find a way to engage with the Swerve in its early days. Building new versions of the same mousetrap will not be sufficient when the historic features of the market start to break down.

Rather, K-12 leaders should:

New value propositions and business models will continue to emerge, and the “winners” of the Swerve will be organizations that innovate from within. Take Acceleration Academies, which enables districts to offer flexible paths to completion for students who might otherwise drop out. Now operating across seven states, their hybrid learning model is emblematic of how businesses can help districts reimagine components of the K-12 experience they traditionally tackled “in-house.”

In the coming years, it’s crucial for K-12 organizations to be agile and responsive to fast-evolving customer needs. Leaders should find the time and space to test new models, even if these may run counter to the core business. Staying relevant in an age of stability is hard enough; finding ways to become durable in a period of transformation is a unique challenge, one that requires both discipline and vision.

Time will tell the true magnitude of the Swerve, but the K-12 community can count on several key shifts:

Depending on where you sit in the ecosystem, this should lead to several questions.

For school leaders, opportunity is at the doorstep, but so is competition. It will be critical to evaluate how market shifts will affect your school community:

For K-12 suppliers, the market will lean on trusted partners to navigate this new terrain. In turn, you should seek to learn the new “DNA” of customers, both districts and parents:

For investors, the balance of power—and contours of TAM—will shift. As you consider and prioritize investment themes, keep an eye on new markets and business models:

As always, we are happy to connect, share additional perspectives, and generate ideas on the key questions above. Please don’t hesitate to reach out to us.