Tyton Partners Voices of Impact Pulse Survey Q3 2023

January 19, 2024 Voices of ImpactThe year 2023 was challenging for the global economy, as it faced multiple headwinds from inflation, geopolitical tensions,…

The year 2023 was challenging for the global economy, as it faced multiple headwinds from inflation, geopolitical tensions, and the ongoing impact of the COVID-19 pandemic. While some regions, such as Asia, achieved moderate growth, others struggled with weak demand, supply bottlenecks, and rising debt. The outlook for 2024 remains uncertain as central banks worldwide grapple with the trade-off between supporting the recovery and containing price pressures. Moreover, regular advancements in artificial intelligence threaten to change how we work.

The impact sector has weathered all these trends and more. But many questions remain about the state of the world of impact at the beginning of 2024. Our Tyton Partners Voices of Impact Pulse Survey sets out to answer some of these questions.

This past October, Tyton partners fielded our second Voices of Impact Survey to a diverse set of impact-oriented stakeholders from across the education ecosystem, including philanthropists, non-profit operators, thought leaders, and other change-makers. The survey tracks these stakeholders’ perspectives, priorities, and challenges as they navigate the rapidly growing and evolving education ecosystem.

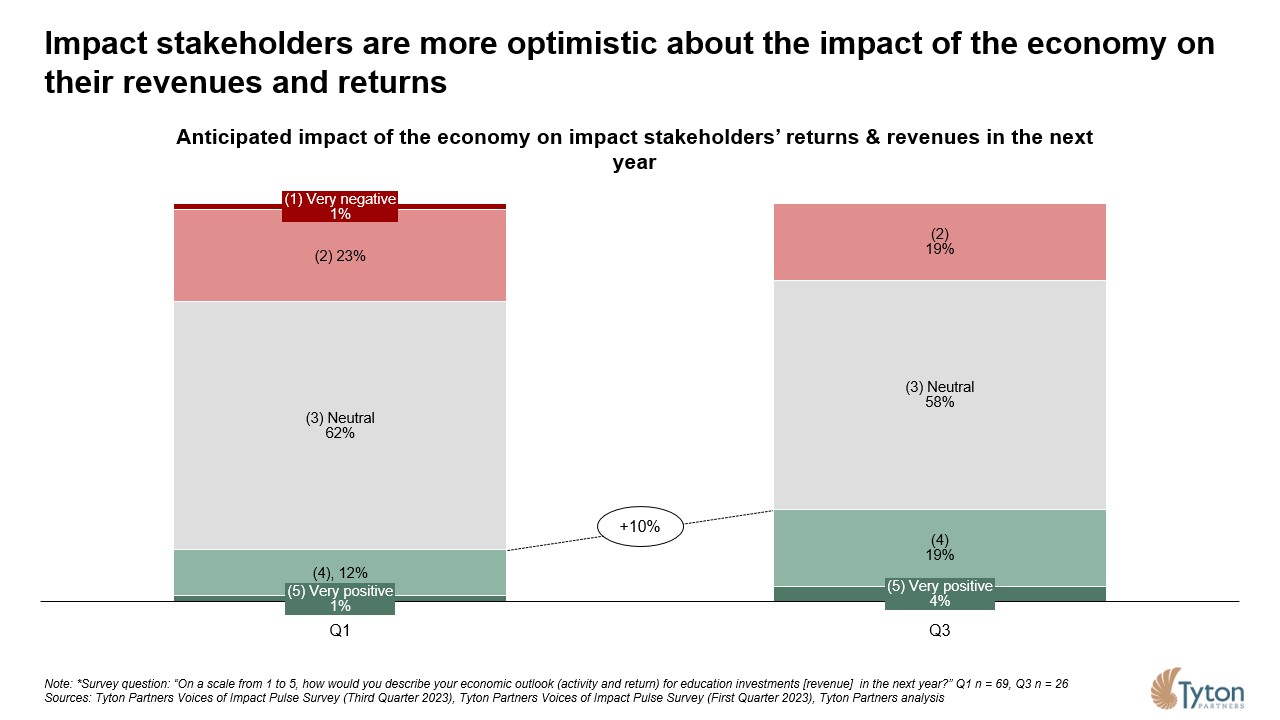

The economic outlook amongst philanthropists has improved since our Q1 study but remains tepid in anticipation of continued geopolitical and economic uncertainty.

Workforce education, skills training, and alternative credentials continue to be an area of focus for impact stakeholders. And these stakeholders are looking toward innovative and experimental approaches to alleviating problems and tensions in these areas.

AI has also begun to be felt in the impact world. However, receptivity toward incorporating AI into the work philanthropists already support is more significant than supporting AI-related programs.

We thank the participants in our second survey and extend a warm welcome to foundation, impact-investing, non-profit, and other impact-oriented leaders in the education sector interested in participating in future iterations; please contact us at impact@tytonpartners.com.

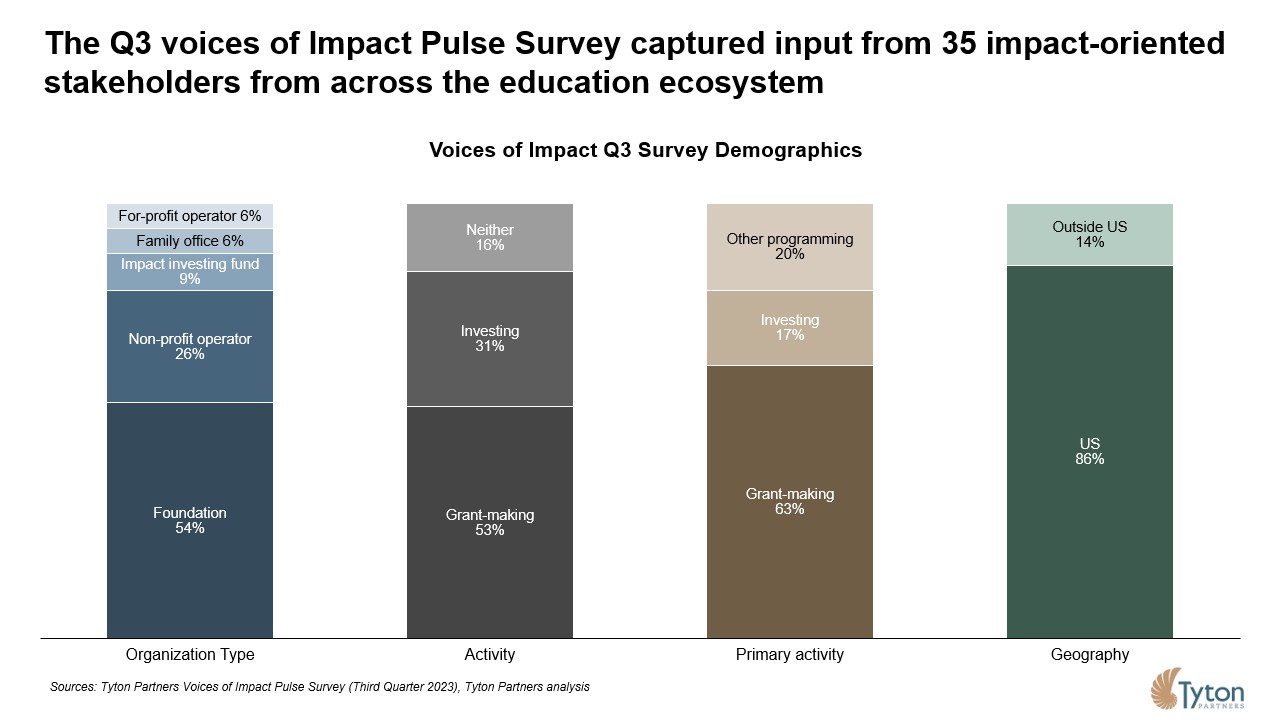

The Voices of Impact Pulse Survey Q3 2023 received responses from 32 stakeholders. Within our sample, respondents came from several organizations, with 54% from foundations, 26% from non-profit operators, and 21% from impact investing funds, family offices, and for-profit operators.

Most respondents came from grantmaking space (63%), although roughly one-fifth of respondents also came from the investing and other programming spaces.

Although the economic outlook of impact stakeholders remains clouded, philanthropists were more optimistic at the close of 2023 than at the beginning. Asking about the impact of the economy on stakeholders’ revenues and returns, respondents were 10% more likely to anticipate a positive impact from the economy in the next year. This is likely due in part to slowing inflation that should lead to stagnant interest rates through the first half of 2024. However, geopolitical instability, an unsure employment market, and a presidential election in 2024 combine for an economic outlook that can just as easily continue steadily or begin to tumble down.

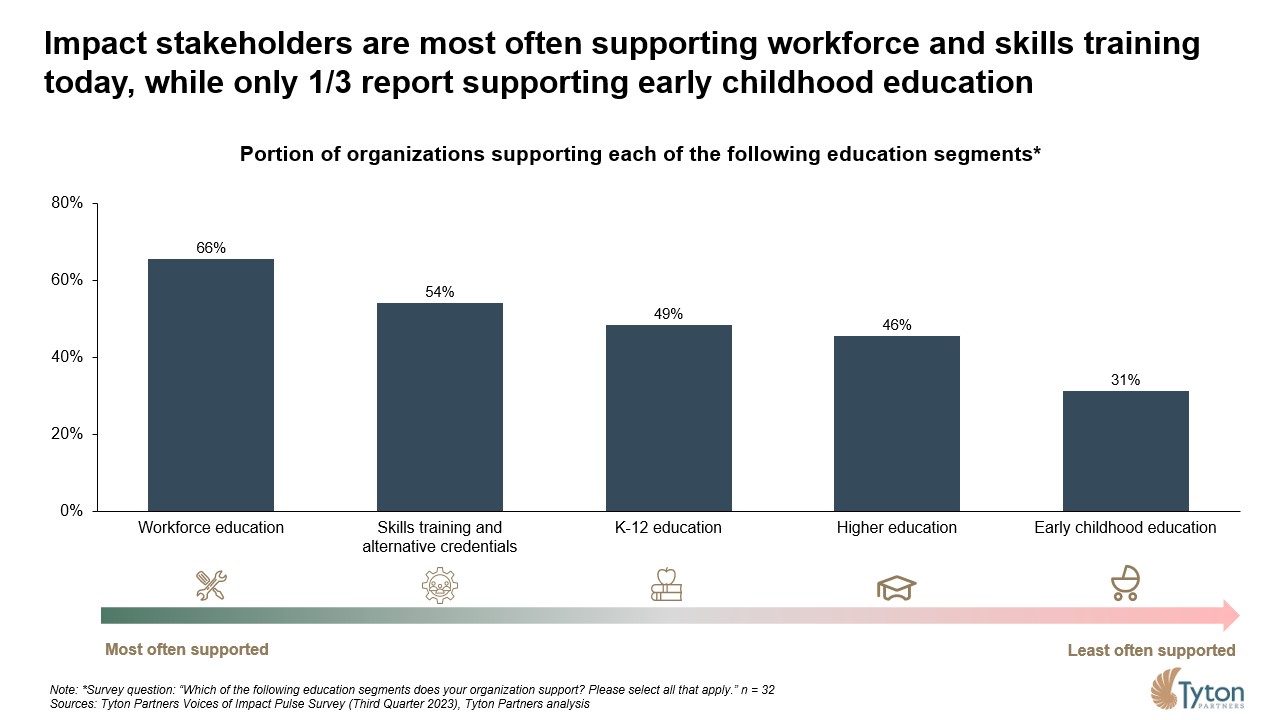

We explored the philanthropic support for different segments of the education sector. We asked our respondents to indicate which areas of education they currently support. Workforce education was the most popular choice, with 66% of respondents expressing their support, followed by skills training and alternative credentials (54%), K-12 education (49%), higher education (46%), and early childhood education (31%).

Our previous surveys have shown similar results, with programs serving workers and learners closer to working age receiving an outsized share of philanthropic support. There is ample evidence that investing in the early years of a child’s life can generate substantial social and economic benefits. Our findings suggest a greater need for grantmaking organizations to consider how supporting early childhood education and childcare can support their broader missions of worker equity.

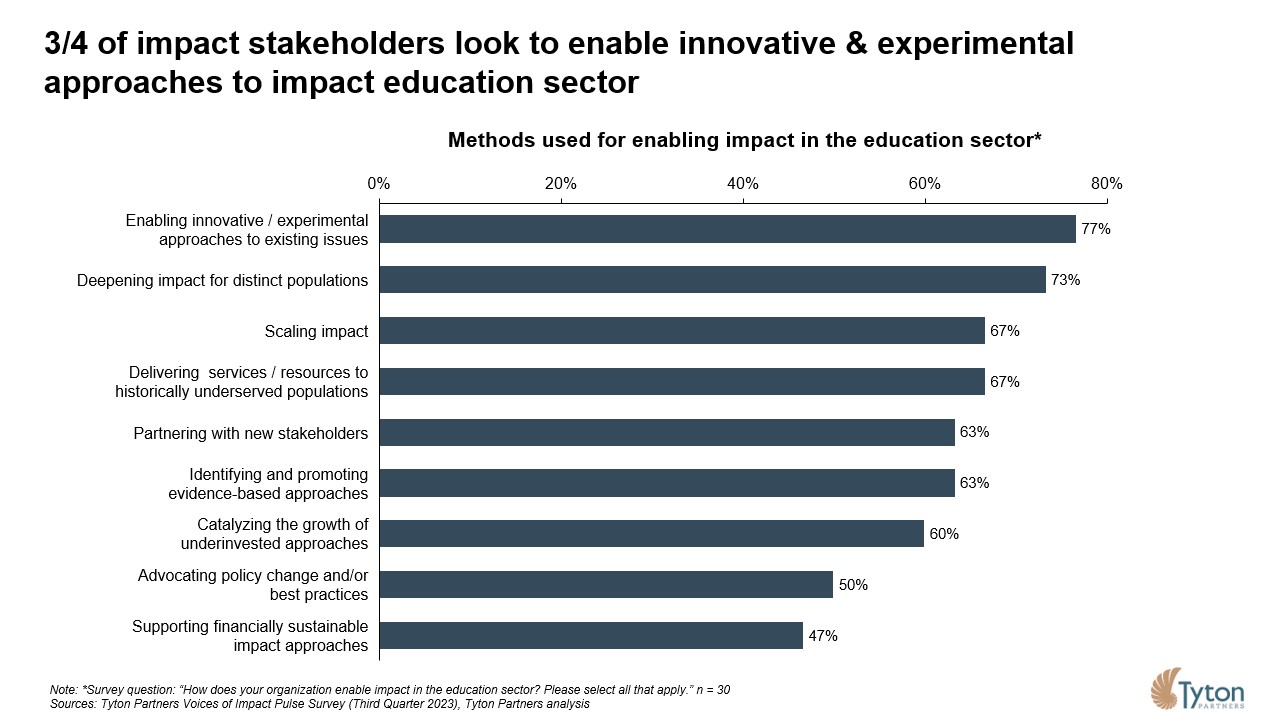

Impact stakeholders in our survey sample reported a strong focus on innovative and experimental approaches to address today’s issues. In a space that has been turned on its head twice in the past three years with COVID-19 and the advent of generative AI, impact stakeholders feel that driving toward more innovation and experimentation is a critical path forward for learners of all ages.

Impact stakeholders are also looking to deepen the impact for district populations significantly affected by the COVID-19 pandemic. Furthermore, with ESSER funds expiring next year, the burden to address learning loss and get students across the US back on track is falling partly on innovative, impact-driven stakeholders willing to invest in radical new solutions.

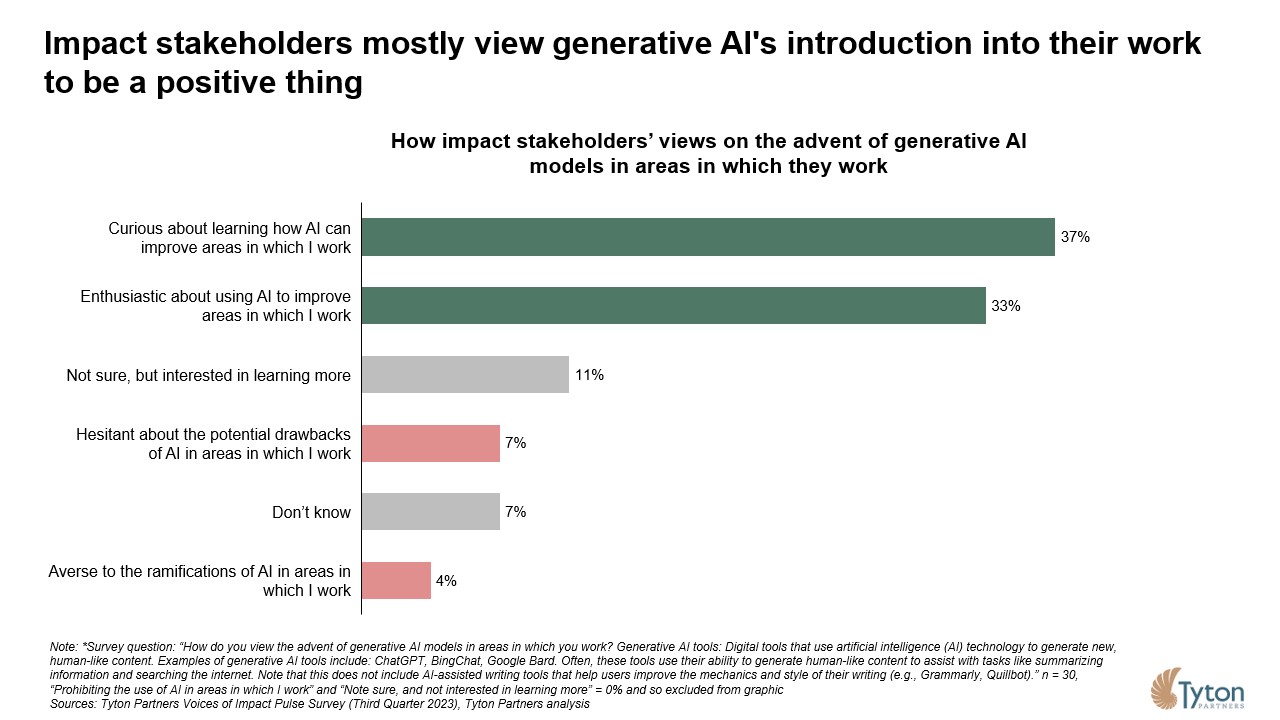

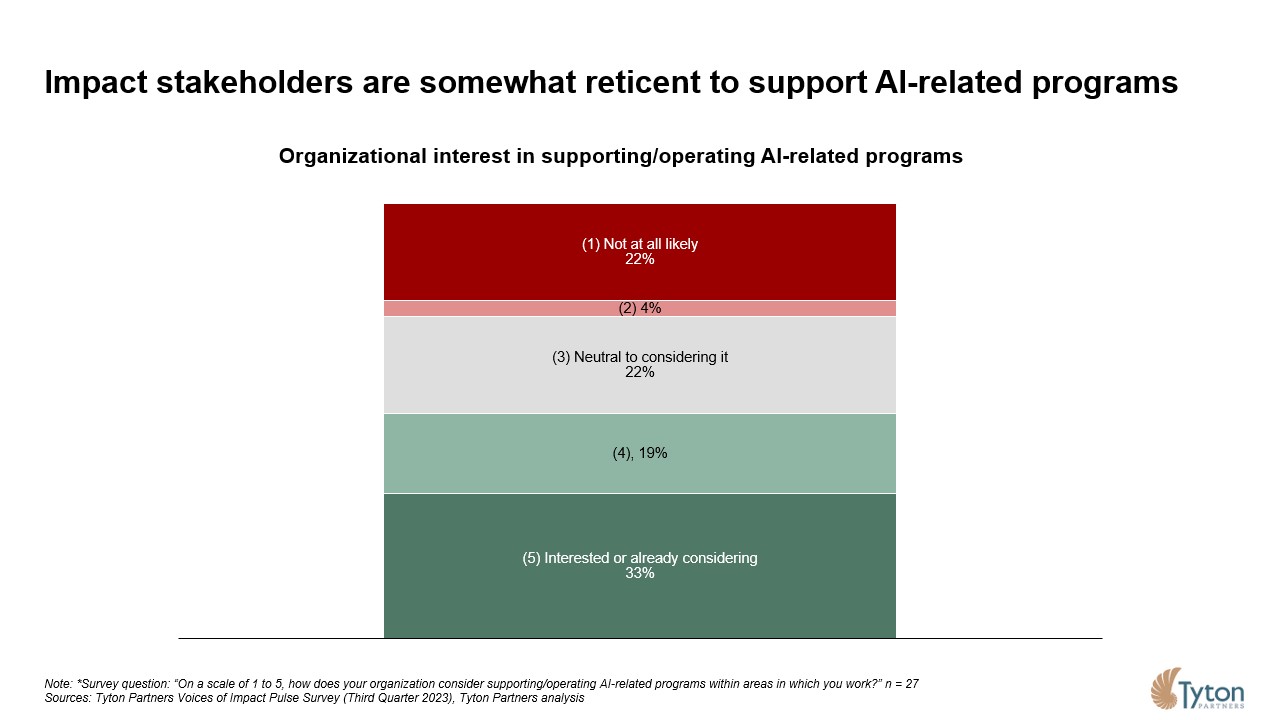

In this 3Q 2023 iteration of the Voices of Impact Survey, we added several questions gauging impact stakeholders’ attitudes toward AI. As a whole, stakeholders are optimistically curious and enthusiastic about how generative AI will improve the areas in which they work. Still, 10% of stakeholders are hesitant or averse to how they anticipate AI will affect their areas of focus. Although philanthropists are mainly excited to see what AI can do, they are less interested in supporting or operating AI-related programs.

This may speak to the general uneasiness and confusion surrounding AI-based businesses and programs. Yet, as impact stakeholders look to enable innovative and experimental approaches to solving the issues of today, AI might be the place they have to invest to do it.

As we turn toward 2024, the preferences and aims of philanthropists will shape the world and education for years to come. As COVID-19-caused learning loss continues to hold students back sometime after returning to school, philanthropists and their grantees will be crucial pieces of the puzzle to make America’s learners whole again. They’ll need to innovate, experiment, and use the best technologies we have access to, but more than that, they’ll need to stay driven and continue striving toward a better tomorrow for learners.

We are always happy to discuss as you and your organization think through these challenges and opportunities. Reach out to have a conversation. If you missed it, here is our Q1 2023 Voices of Impact pulse survey.