H1 2026 Education Sector Deal Recap: The Rebound, Realized – Unevenly

July 20, 2026 BlogIntroduction Our last two updates highlighted a similar story. In July 2025 we described a transaction market that…

For the past three years, our team has had some version of the same conversation: Is the K-12 market turning a corner? The honest answer, at least for the institutional market, is probably not. Public school enrollment is in structural decline, budgets remain tight, and rapidly changing expectations around technology and the workforce cause district priorities to shift faster than procurement cycles can track, adding to the uncertainty providers encounter. This amounts to a market that is harder to win in; business leaders who internalize these dynamics are best positioned to respond.

At the same time, opportunities do persist. District demand is more measured, concentrating on a more defensible list of priorities, but it has not retreated. District leaders still need effective partners to help them demonstrate measurable student progress, address disenrollment challenges, and enable operational efficiencies, among other issues, in a manner and at a pace that reflects their capacity and risk tolerance. New customer acquisition is difficult, but it persists.

In this month’s newsletter, we draw on a recent a pulse survey of more than 150 superintendents, tracking how their priorities, sentiment, and purchasing behavior are evolving. The findings offer a ground-level read on where districts are this selling season; three themes stand out for providers as they seek to win in the current environment.

Below, we unpack each of these three themes and offer perspective on the implications for providers navigating this market.

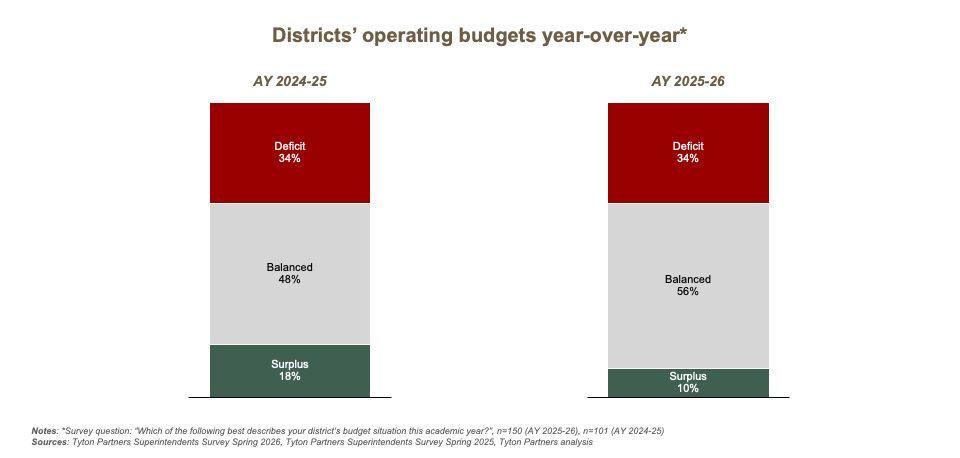

The K-12 market has absorbed its post-ESSER setbacks and reset around a narrower, more defensible set of priorities. The underlying budget environment remains a consistent driver of this pressure. This spring’s pulse survey indicated 34% of district superintendents report an operating budget deficit – consistent with last year’s feedback – but a smaller percentage than last year report a surplus (i.e., 10% compared to 18%). While many hoped for a stronger bounce-back given the market volatility last spring/ summer, the data suggests a somewhat stable market environment that continues to face budget pressures.

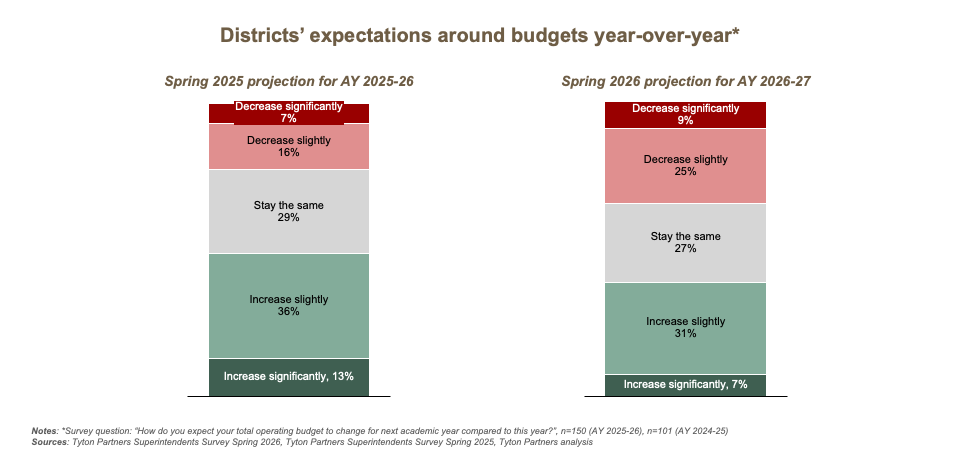

Currently, 38% of district leaders anticipate their AY26-27 budgets represent a year-over-year increase, while 34% report a further decline. Navigating this variability – and the pressures districts continue to face – is a situation most providers should expect to face this summer, and one that warrants a clear course of action for districts on either end of the spectrum.

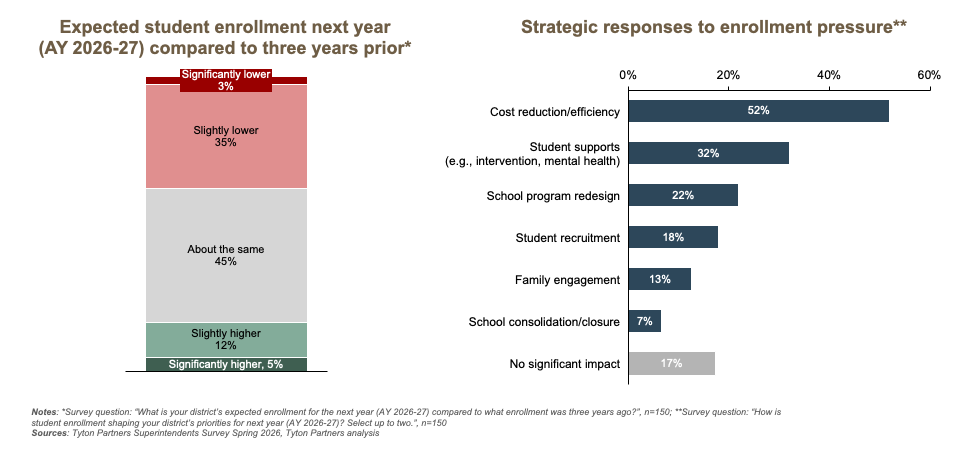

Enrollment trends are a critical part of the problem. Nearly 40% of district superintendents report enrollment declines, a dynamic that directly erodes per-pupil funding and, with it, the resource base districts have to work with. The response is bifurcated: roughly half of respondents are cutting costs (52%), while others are investing in stronger systems of support (32%), redesigned programs (22%), or active recruitment (18%) to stem the outflow. In these cases, enrollment pressure is becoming a buying trigger. Providers who can draw a clear line between their solutions and a district’s ability to (re)enroll students will find that enrollment pressure can open doors this cycle.

Taken together, the budget and enrollment picture points to a market that could remain challenging. As today’s fiscal pressures evolve from a temporary post-ESSER correction into a sustained operating reality, the market will increasingly reward providers who can demonstrate outcomes, justify their place in a leaner vendor portfolio, and embed within core workflows.

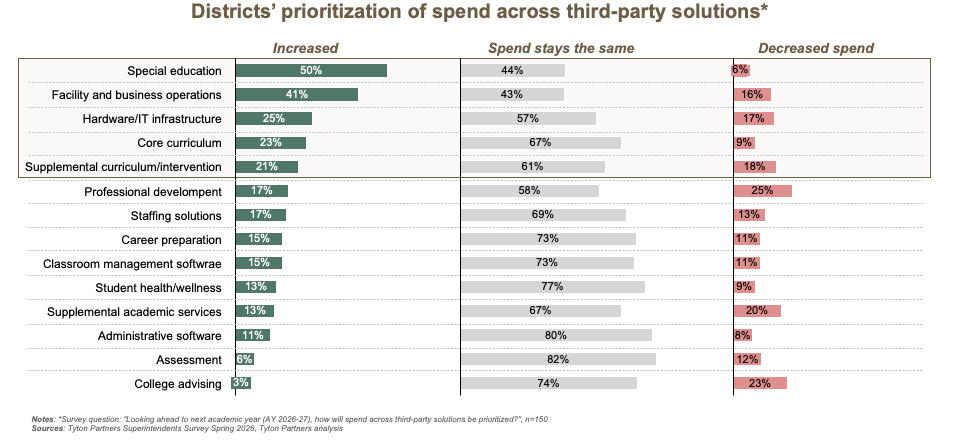

The factors creating pressure on districts are also clarifying where buying appetite and momentum remains strong. Districts are actively (re)allocating resources to categories and solutions tied to measurable student academic growth, realized operational efficiency, and educator effectiveness. For providers, this is where deals will happen this cycle.

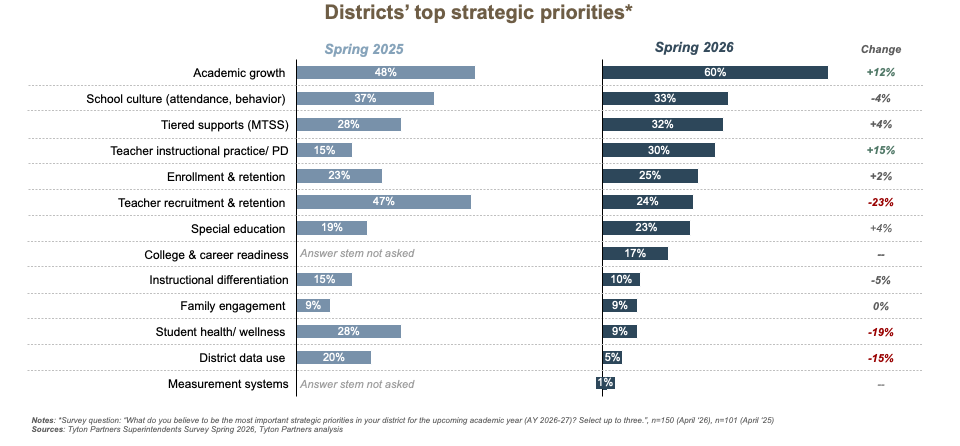

Post-COVID, academic outcomes have returned as districts’ defining priority, as highlighted below. At the same time, the doubling of teacher development as a priority year-over-year (i.e., from 15% to 30%) highlights the upskilling needs that persist, particularly in conjunction with the wave of HQIM adoptions and resets that states and districts are pursuing. High-profile HQIM + teacher development initiatives like NYC Reads and Solves reinforce that new instructional materials are the easy part of the equation.

A (re)centering on academic outcomes and instruction is driving spend towards categories of direct student impact – curriculum, intervention, and special education. Compliance mandates and dedicated funding make these categories among the most durable in the market, but this also attracts more competition. The curriculum landscape is more crowded than ever, and early signals from California suggest that an abundance of options can further slow procurement. Winning in the curriculum and special education markets requires a sharper view of where the likelihood of success is strongest. Providers who define those segments clearly and let go of others predisposed to a different approach will convert more of this demand into revenue.

Operational improvements and efficiency are also embedded as a second major spending lens. One of the largest areas receiving increased spending consideration is tied to facility and business operations. And, a sizable percentage of districts anticipate expanding investments in their hardware and IT infrastructure. Districts are not looking to run fewer operations, but they need to run them better, and providers who can reduce administration burden or deliver measurable cost offsets are well-positioned to win.

The through-line is accountability. Districts are increasingly required to demonstrate outcomes, justify dollars, and control costs. For providers, products that sit outside core instructional or operational workflows could be at a structural disadvantage this cycle. More broadly, discretionary spending will continue to face intense scrutiny, and district leaders are operating with minimal margin for error. Products or services that lead with a clear, direct benefit to students or operations will have a distinct advantage moving through procurement.

A consistent pattern runs through our superintendent survey: districts have identified clear priorities, but lack the capacity to execute against them. Providers who close that gap – pairing solutions with strong implementation support and aligned incentives – have the clearest opportunity to differentiate and build momentum in this market environment.

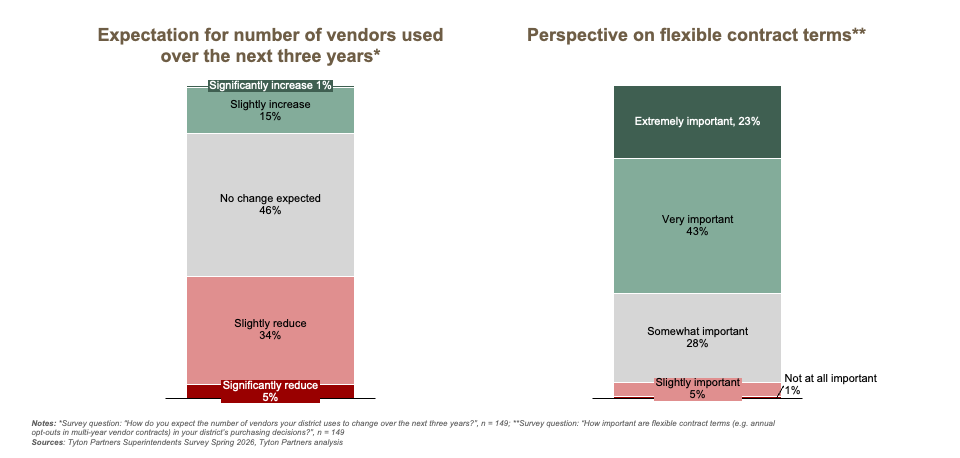

This gap is shaping the procurement environment. Nearly 40% of districts expect to reduce vendor count, signaling a market that is more likely to end relationships than start new ones. Moreover, 66% rate flexible contract terms – including milestone-based agreements and outcomes-based contracts – as important decision factors. Districts are looking for fewer, better partners who will deliver and help them manage against their critical priorities.

Three areas stand out where this capacity gap is widest – and where providers who show up with the right solutions and implementation playbooks will find the most durable footing.

Enrollment: As districts find themselves needing to compete more effectively for enrollment, the ability to drive retention and (re)enrollment becomes an active buying trigger. With nearly 40% of districts reporting declining enrollment due to school choice competition and demographic declines, traditional assumptions about how to fill seats no longer hold. Districts are responding – through program redesign, active recruitment, and deeper family engagement – but remain underprepared. Tyton Partners’ Choose to Learn 2026 report surfaces a persistent tension: the activity districts have pursued has not translated into better outcomes, and execution remains the gap. Providers who can help districts move from intention to measurable impact – building capabilities that retain families and attract new ones – are addressing one of the market’s most significant unmet needs.

Teacher practice: Districts are signaling that they want more effective teachers but are spending less to develop them. In our superintendent survey, teacher instructional practice has jumped 15% as a strategic priority year-over-year (2025 to 2026), but professional development is simultaneously the top area of reduced third-party investment – a tension that federal funding uncertainty has made harder to resolve. Given this dynamic, providers who embed teacher-facing capabilities into their core offerings reframe the investment entirely and sidestep this budget tension. The AI dimension is central to this issue: 59% of districts identify teacher planning and productivity as a top priority for expanded AI usage, but staff capacity remains a barrier to adoption – a dynamic our forthcoming publication on K-12 student success will explore in greater depth. Providers who pair AI-enabled teacher workflows with hands-on implementation support are positioned at the center of this market tension and can turn it into a competitive advantage.

Operational efficiency: Finally, district leaders recognize that operational efficiency is critical, but restructuring workflows or consolidating vendors is itself a significant capacity problem. Most lack the bandwidth to reshape their procurement around more strategic, system-wide partnerships, and measuring the resulting cost and time savings compounds the challenge. Moreover, managing transportation networks, food services, and facility operations are enterprise-level challenges that consume bandwidth districts would rather direct toward teaching and learning. Increasing, outsourcing these functions is how forward-thinking districts are reclaiming this focus. Providers who take on that complexity alongside districts – helping them shed operational weight, consolidate procurement around strategic priorities, and quantify returns – will distinguish themselves as partners worth keeping as districts make difficult tradeoffs.

The K-12 market has reorganized. Districts are adjusting to the post-ESSER funding environment and striving to do more with less or the same. Buying continues, but on tighter terms: clearer proof of outcomes and a higher bar for execution.

For providers, this is both a mandate and an opening. The mandate is precision: clear value, fit, and evidence that purchasing decisions hold up under scrutiny. Districts need partners who can help them improve academic outcomes under accountability pressure, build teacher effectiveness into the tools they already use, and navigate a technology landscape that is evolving faster than they can absorb on their own. Strategies built for a different K-12 environment will not suffice. But providers who make it easy for districts to justify purchases today are positioned well for the future. As structural pressure persists, districts will draw on partners they trust to help them reinvent how they operate and deliver on their core mission. Forming trust this cycle amount to enduring opportunity over time.

If you’d like to discuss the implications of these findings for your positioning or go-to-market initiatives, contact us to schedule a conversation.